The Global AI Divide and the Global South’s Choice

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

The US–China AI split is becoming structural The Global South must secure access without accepting permanent dependence Cheaper AI matters only when it builds local capacity and bargaining power

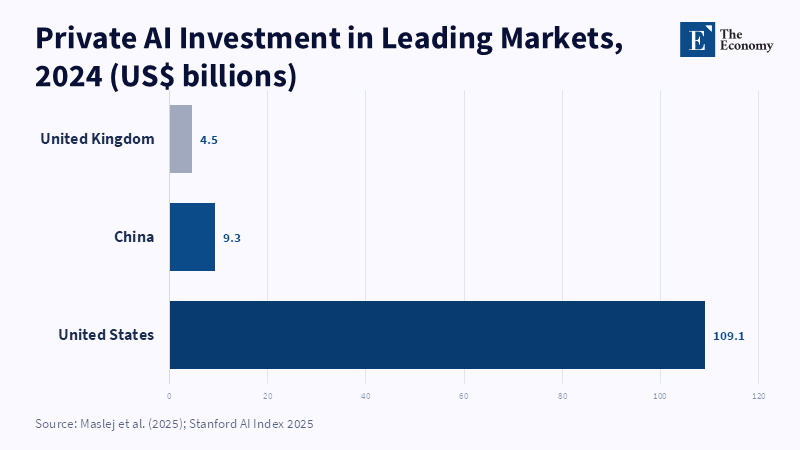

The global AI divide is often reduced to a gap that can be closed with better funding and broader access. The harder truth is that the divide is hardening as a structure. By 2024, private AI investment in the United States had reached $109.1b, almost twelve times as much as China's $9.3b. But leading Chinese models moved close to US performance on major benchmarks and its firms pushed cheap, competitive, more open systems into the marketplace. This is not a conventional development gap. This is a contest between two parallel technological systems of individual firms, each built around different firms, chips, cloud systems and political aims. Efforts to integrate them into a neutral global order are unlikely to go anywhere and the practical challenge is different. The Global South cannot treat access as the ultimate goal. It has to use the race to drive down prices, open standards, local talent, control over data and the freedom to switch vendors.

And that reframing matters because the global AI divide has two separate issues. The first is the strategic gap between the United States and China. That is a gap based on security, industrial policy and control over critical technologies. That divide will not disappear through calls for a common global standard. The second is the gap between countries that have AI infrastructure and those that rent it. That gap can still be shaped. The approach then should accept strategic competition while resisting technological dependence. The purpose is not to produce a frontier model everywhere. It is not to stay neutral in all battles. The idea should be to make the choice of cloud, chip, model, or lender's infrastructure a non-permanent choice.

The Global AI Divide Is Not One Divide

The US and China are seeking rival AI positions because power derives from leadership, which exerts military, economic and political influence. US export controls established in 2022 and reinforced in 2023 and 2024 restrict China from accessing the latest chips and manufacturing equipment. China has responded by boosting homegrown chips, state data infrastructure, local cloud providers and models designed to compete despite restricted access to advanced hardware. The result looks like other lengthy strategic rivalries. The Cold War with the arms and space races warned that competitors' contrasting technical tracks often continue side by side until one falls behind. AI may not produce one definitive winner; firms can lead in chips, models, clouds and applications. Clashing standards and supply chains linger. They delay research and escalate price tags. They also stem from the rivalry's very reasoning.

Each side fears that mutual dependence will afford the opponent the upper hand. No universal appeal can erase that worry. A single, indeed cheaper AI would be one global system, but neither major driver prefers efficiency to command. The numbers reveal why the rivalry will endure. US-based organizations created 40 of the important AI models in 2024, compared to 15 from China and three for Europe. China retained the lead in AI publications and patents and the performance gap on key model tests shrank to close to a dead heat. Meanwhile, 100 firms, mainly based in the US and China, represented 40 percent of global corporate AI R&D in 2022, while just two nations held 60 percent of AI patents and generated around one third of AI research articles. This is a strategic race, not a joint public project. The most likely result is not one uniform standard adopted by calm global consensus, but a long timespan of overlap, extension and partial separation, then hegemony in some aspects and rivalry in others.

That does not mean every country has to make one absolute decision. AI is a stack. A government can use US cloud services, Chinese network equipment, open-source models, domestic data centers and national open-source software. While security restrictions could restrict this choice, it is still more variable than a bloc map. And therefore, the policy’s relevant scale becomes the layer, not the nation. How much reliance on outsiders can a country accept? When are two suppliers advisable? How much control must be public? Perhaps health records need local hosting; maybe farm planning can run on a cheap foreign model; perhaps climate defense needs an unquestionable national-stack. To treat all three as equal is to hand a bargaining advantage away.

Why Waiting Will Widen the Global AI Divide

Waiting for prices to fall clearly makes a lot of economic sense. AI has come down drastically in price. It cost roughly US$20 per million tokens to use a GPT-3.5 performance-level model in November 2022 and only $0.07 by October 2024, a decline of more than 99 percent. Hardware costs are also sliding and smaller models are producing usable results on mundane hardware. Open-weight models' about 8% performance gap with closed models has shrunk to 1.7 percent in a year. DeepSeek-V3 showed a way engineers can reduce the reported cost of a large training run to approximately $5.6 million, but without earlier research and testing included. For cash-crunched states and companies, waiting to buy in and repurpose proven tools may prove smarter than jumping into a costly technology frontier.

But the used-car analogy fails most where it counts. The used car is a finished asset. AI is a live service that depends on updates, cloud connectivity, software tools, security patches, data flows and technical support. Even a lower-cost version does not eliminate the need for electricity, connectivity, knowledgeable staff, local data and a place to run it. For some, a lower-cost model of an AI software service may also increase dependence on the hosting firm. Cloud contracts can be locked in with prices for migration, proprietary software and high data-export charges. A country that places an order immediately may pay less per query, but at the cost of not being able to replace the provider, review the underlying system, or create local companies around it. The falling price of something does not alone confer market power.

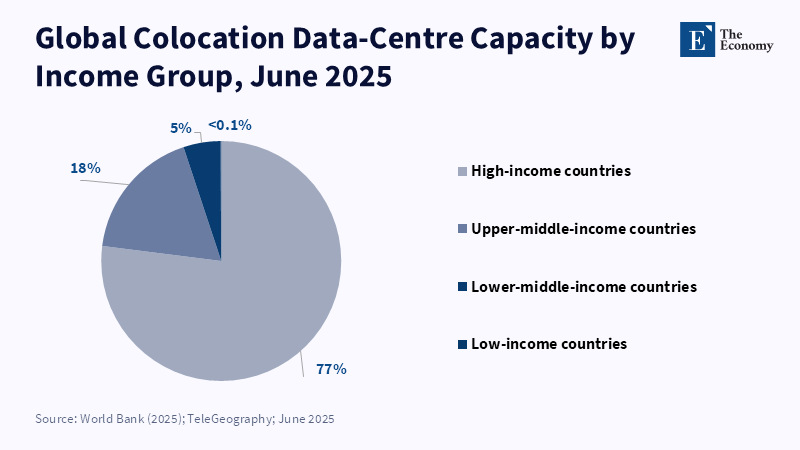

The infrastructure divide makes the option to passively wait even more dangerous. High-income countries owned 77 percent of the world's colocation data center capacity by June 2025. Lower-middle-income countries owned 5 percent; low-income countries owned less than 0.1 percent. High-income countries also stored 97 percent of the capacity in the top 500 high-performance computing infrastructures in the world. Middle-income countries kept just 1 percent of this capacity without China and India, even though they comprised 48 percent of the world's population. Connectivity, too, remains unequal. In 2024, roughly one-third of the world's population remained unconnected to the Internet and median internet speeds were still below 25 megabits per second for low-income and lower-middle-income countries. Cheap AI cannot bridge this global AI divide unless the network is fast, the power supply is reliable and the data center is close by.

The Global AI Divide Requires Choice Without Submission

The Global South-and "the South" more broadly-will have to make tradeoffs. Public agencies can't buy every cloud, can't run every model, can't accommodate the competing demands of rival security architectures at the same time. A country with high-speed demand for chips, loans, data centres and digital public services will feel pressure from both sides. The error is in elevating a legitimate pragmatic procurement choice into an irreversible commitment. A contract to buy compute shouldn't simultaneously hand over vast rights over public data. A discount on one model shouldn't mean the exclusion of a competitor. A data-centre purchase shouldn't mean a final blow to independent assessments or require public systems to adopt a single vendor's operational tools. Tomorrow's choices are unavoidable. Choices may be unavoidable, but lock-in is not. That distinction should guide every deal involving cloud migration, public data and digital identity systems.

So many middle powers are already experimenting with a more limited version of this autonomy. India initiated the IndiaAI Mission in March 2024 with a budget of ₹103.72 billion, approximately US$1.25 billion and an initiative for the state accessibility of 10,000 or more Graphics Processing Units. Brazil's 2024-28 plan for AI proposed nearly R$23 billion for infrastructure, public services, business innovation, skills and a national language model. The African Union adopted a continental AI framework in July 2024 that prioritized domestic capacity, data governance, skills and regional collaboration. None of these initiatives can match the frontier investment of the US or China. That is not the test. Their significance is in establishing bargaining assets: shared compute, indigenous expertise, public data regulations and a market that can articulate its needs better.

An effective policy would be one of adaptation, not imitation. Developing countries don't need to build a frontier model. They do need the ability to test models and bring them to a specific task, run low-resource subsets of the system and swap out one provider for another. Local language support will be critical. In 2025, English was around 45 percent of the web and half of open data on one leading AI platform in 2024. A model may be cheap and powerful, but still doesn't get the local language, legal system, crops, diseases or the country's archive right: the money you save is wasted if you get bad answers, poor local fit. Therefore, public policy should support local data sets, evaluation infrastructure, translation tools and task-specific models before national-winner projects.

Regional action bolsters this approach. A lone state has limited leverage in negotiations with a global cloud provider and model provider, but a regional bloc can pool demand, negotiate as an entity on common contractual terms and back shared testing facilities. This bloc can define data portability and open APIs, transparent pricing, audit capabilities and advanced notice of service withdrawals. It can segment infrastructure thoughtfully. Not all countries need large data centres, but every country needs a reliable connection to regional compute and policy to protect sensitive data. Regional buy-in does not eliminate political pressure but it does increase the cost of undesirable terms and mitigate the probability that one bilateral arrangement will define policy across an entire market. Common rules and standards can also facilitate the cross-border sale of products without re-engineering them.

Turn the Global AI Divide Into Bargaining Power

Both the US and China have an incentive to make cheaper AI available to developing markets. It is not an act of charity. Wide adoption will expose technical standards, attract developers into its ecosystem, increase feedback loops and raise demand for related cloud, chip, payment and software services. A provider can absorb low margins at the model layer if it pulls in revenue and influence elsewhere. China's open cheap model approach can reach elsewhere, even as its own cloud share remains relatively small. US firms leverage their extensive deep-cloud networks, robust developer infrastructure and sizable capital resources to counter China's approach. In both cases , affordable access is a strategic play to shape future reliance. This same principle has driven past conflicts over operating systems, telecom infrastructures and digital payments.

This creates a foothold. Governments should view the above initiatives and additional discounts as bids for entry. The cost to enter should include the provisioning of more than free accounts: tests of local language performance capabilities to qualify deals; training for public staff; assistance to establish local start-ups; transparent data & licensing terms; and control over platform migration. Large public contracts should have exit clauses and open technical interfaces. Public data should not be remixed into datasets for general-purpose model training without ongoing voluntary consent and public benefit. Tax breaks to data centres should be considered conditional on power investment, building local vendors and measurable improvements in service levels. It is not about punishing foreigners. It is about turning short-term entry into a platform for sustained local capability. Do all of this before market leadership is internally subsidized, not after.

Others will say conditions push up prices and slow innovation. That is not incorrect. Complex negotiations require well-resourced staff and protecting weak domestic providers through strict local hosting requirements adds cost and does not necessarily improve service. The answer is not to scrap conditions, but to keep them targeted, consistent and based on identifiable risks. Conditions such as portability of data, privacy with contractual protections, audit rights and open transparent pricing are not optional extras. They are directly comparable to unfair charges levied under strong commercial contracts and reciprocal rights set out in a well-informed bargain. Proportional sharing of private sector technical teams and use of model regional contracts can help keep costs to the government down. The government should not mandatorily require local hosting for each application. Specific applications may need it, most applications will not. Wise policy balances true sovereignty needs and expensive symbolism.

The global AI gap will not close by one side winning and by offering its old technologies to the South at a discount. It will not close by any global agreement that brokers two competing nations to abandon the pursuit of control. The critical issue is whether cheaper access will make developing economies more empowered or merely more dependent. Falling prices of models are helpful. Open-weight models are helpful. Foreign data centres and cloud credits are helpful. Each should be weighed against what endures after the discount ends. Does the nation have skilled personnel, portable data, local testing systems, dependable network connections and more than one seller? Absent that, access may widen while the underlying structural divide may continue to deepen. The aim of the policymaker, then, is not to end the US-China competition. It is to negotiate inside it, develop options below it and make sure that the southern world moves into the upcoming period of AI as a customer with bargaining power rather than a dependent market with no credible alternative.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

African Union Commission (2024) Continental Artificial Intelligence Strategy: Harnessing AI for Africa’s Development and Prosperity. Addis Ababa: African Union Commission.

Bureau of Industry and Security (2023) ‘Commerce strengthens restrictions on advanced computing semiconductors, semiconductor manufacturing equipment, and supercomputing items to countries of concern’. Washington, DC: United States Department of Commerce.

DeepSeek-AI (2024) ‘DeepSeek-V3 technical report’, arXiv, 2412.19437.

Government of Brazil, Ministry of Science, Technology and Innovation (2024) Brazilian Artificial Intelligence Plan 2024–2028: AI for the Good of All. Brasília: Government of Brazil.

Government of India, Press Information Bureau (2024) ‘Cabinet approves ambitious IndiaAI Mission to strengthen the AI innovation ecosystem’. New Delhi: Government of India.

Maslej, N., Fattorini, L., Perrault, R., Gil, Y., Parli, V., Kariuki, N., Capstick, E., Reuel, A., Brynjolfsson, E., Etchemendy, J., Ligett, K., Lyons, T., Manyika, J., Niebles, J.C., Shoham, Y., Wald, R., Walsh, T., Hamrah, A., Santarlasci, L., Betts Lotufo, J., Rome, A., Shi, A. and Oak, S. (2025) Artificial Intelligence Index Report 2025. Stanford, CA: Stanford Institute for Human-Centered Artificial Intelligence.

Signé, L. (2026) ‘How to bridge the global AI divide’. Washington, DC: Brookings Institution.

TeleGeography (2025) Data Center Research Service. Washington, DC: TeleGeography.

United Nations Conference on Trade and Development (2025) Technology and Innovation Report 2025: Inclusive Artificial Intelligence for Development. Geneva: United Nations.

World Bank (2025) Digital Progress and Trends Report 2025: Strengthening AI Foundations. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.