Trade Policy Uncertainty: The Hidden Tax on Foreign Investment

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Trade policy uncertainty deters FDI more than predictable barriers Lower-income and highly integrated economies face the largest losses Stable rules have become essential investment infrastructure

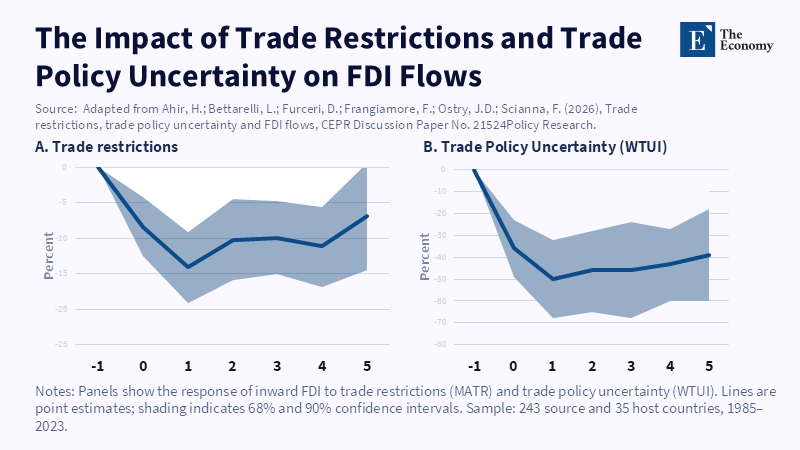

An increase in trade policy uncertainty similar to that following the Brexit vote can simultaneously cut foreign direct investment by an amount equal to roughly 40% of its sample mean. And the cost could increase to around 50% after a year and stay for at least five years thereafter. The result should influence policymakers' attitudes toward trade restrictions. A duty refers to a published value. A technical regulation refers to a written test. Uncertainty has no unit; yet it can inflict a greater burden. It causes firms to hold back, minimize projects, relocate them, or cancel them without any public notice. The effects occur prior to or while trade drops and a plant closes. They happen at the moment when a director determines that a country's policies may not be sustainable for the investment. Countries compete not just on taxes, salaries, natural resources, or shipping routes. They also compete on the anticipated duration of their commitments.

Trade Policy Uncertainty and FDI: Why Waiting Becomes Rational

The 2026 US-Iran conflict was therefore instructive. The United Arab Emirates was not on the front line yet air and shipping hazards change rapidly in the Gulf. European aviation regulators, for example, kept the Emirates airspace decision region so active that conflict was identified in June. This did not mean the Emirates were not a good investment, but it did demonstrate how a local incident can change a risk model in a matter of days. The costs of insurance go up. Travel planning by air is amended. Supply routes are less secure. In fact, war risk may ease just as quickly. A government-imposed barrier to trade has a different lifetime. It may last for a full term, become associated with lobbying and outlive the officials who put it there. For semi-permanent capital, that policy lifetime may be more important than the initial impact.

FDI is vulnerable because it is costly to exit. If, say, a company issued a bond or an import order, it could take the hit. It would not be so easy to relocate a factory, warehouses, a data center, or a network of suppliers. These projects involve sunk costs. Once incurred, much of the expenditure is irrecoverable. This explains why postponement is not necessarily mismanagement. When the future trade regime is ambiguous, the value of patience can be high. During this period, the company can keep its powder dry until it discovers whether a tariff is going to go up or down, whether the local-content mandate will make life harder, or whether the renewal of its license will be granted. Effective trade policy uncertainty acts as a stealth border tax. It demands a higher rate of return from investors even before the formal tariff instrument has been ratcheted. Consequently, large companies choose to play the long game while smaller outfits might lack the capital buffer to stand the strain.

The world figures show why this is relevant now. UN Conference on Trade and Development reported that the underlying real productive foreign direct investment declined by 11 percent in 2024, apart from the often instability-producing conduit flows. Provisional estimates pointed for 2025 to a total value, a 14 percent headline growth to approximately $1.6 trillion. More than 140 billion dollars of this growth was in conduit flows through financial centers. Excluding those flows, the rise was only about 5 percent. Other indicators were less promising, as the international project finance declined in value by 16 percent and the number of new greenfield investments dropped by 16 percent. This was not a broad investment boom. It was a small and thin recovery led by a handful of large investments in capital-intensive sectors. Therefore, an economy that introduces trade policy uncertainty competes for a smaller and more selective pool of increasingly cautious capital.

A Trade Barrier Can Attract a Factory-and Still Weaken FDI

Not all trade restrictions discourage all types of FDI. Certain restrictions can actually motivate firms to manufacture within a protected host country – the classic tariff jumping effect. Evidence of technical barriers in Central, East and South East Europe suggests that while there were some trade barriers that induced international companies to produce locally rather than export, others were investment-friendly as they proved product quality or allowed easier application of a new legal framework. This is relevant because regulation is not identical to protectionism. Food safety standards, product testing, environmental and common standards can also solve real problems and a country with trusted standards may prove more attractive than a country with a fragile control system. The question is not whether a state regulates – it is whether the regulation is predictable, non-discriminative, consistent and accessible to both national and foreign competitors.

Tariff-jumping is therefore more limited. It is most appropriate for firms that wish to sell within a large protected market and that are able to replicate most of the activity there. That logic ignores much of the complexity of modern supply chains. A single product might be imported from five nations, make use of foreign software, depend on regional transport and then export the bulk of its output. A tariff on that final good then encourages local assembly. A tariff on imported inputs, intellectual property rights, standards, licensing, or bottlenecks to future market access may end up killing the whole project. A single applied rule might entice one plant but free several potential supplier projects. It may also favor Goliath incumbents who will be able to support a number of duplicate internal systems and legal departments, thus presenting entry hurdles for the smaller players with much higher fixed costs. Consequently, trade policy is also to be examined not only from the spotlight of the one or two proposed factory deals, but across the entire pre- and post-production stages involved in a particular project.

The difference with the most recent evidence is huge. An increase of one standard deviation in trade barriers leads to a 10% of mean sample immediately and to about 15% of mean sample after a year of decline in FDI. An increase of one standard deviation in trade policy uncertainty leads to a decrease in FDI by about 40% immediately and by about 50% after a year. A predictable restriction can be priced, but an opaque rule cannot. Firms may manufacture a new good in compliance with a fixed standard, but they cannot prepare for a constantly moving rule. In fact, security or resilience concerns may still justify screening, export restrictions, or local capacity constraints. But security does not require chaos. A clearly articulated, narrow rule is less costly than an arbitrary, process-dependent standard.

Policy Durability Is the New Investment Infrastructure

Governments sell roads, ports, tax credits, industrial land and talented workers. Those things matter. But they will not be enough. The closer production gets to being broken up internationally, the more your fundamental advantage is how long your policies last. Investors need certainty about whether they will be able to import pieces, transfer data, repatriate earnings, renew their licenses and sell into nearby markets. And they need to know how quickly those policies can change. The rise of political-risk advice is a market reaction to this need. Companies now pay for country forecasts, sanctions screening, war-and-peace calculations and rule monitoring before mobilizing funds. Yet this investment does not eliminate risk. It proves the point that volatility has become a standard project fee. A polity that makes its policies equally opaque transmits the costs of bad public policy onto private balance sheets.

Sovereign policy can be endured without forever assuming it. Large-scale trade and investment policies should be time-stamped, require publication and subject themselves to a credible impact test. Projects currently underway should be given a predetermined window of transition unless immediate compliance would dissipate sunk investment. Short-term policies should sunset unless reaffirmed by measure within a designated reevaluation period. Emergency powers should specify the circumstances that trigger and terminate the powers. Regulatory agencies should provide notices and definitive answers to enforcement questions by standardized deadlines. Statutes should impose a reasonable authorization period before limitation periods and challenges should not lock in expensive litigation or treaty settlement. These measures do not prevent policy shifts any more than imagining war. They force reflection into an unambiguous time horizon.

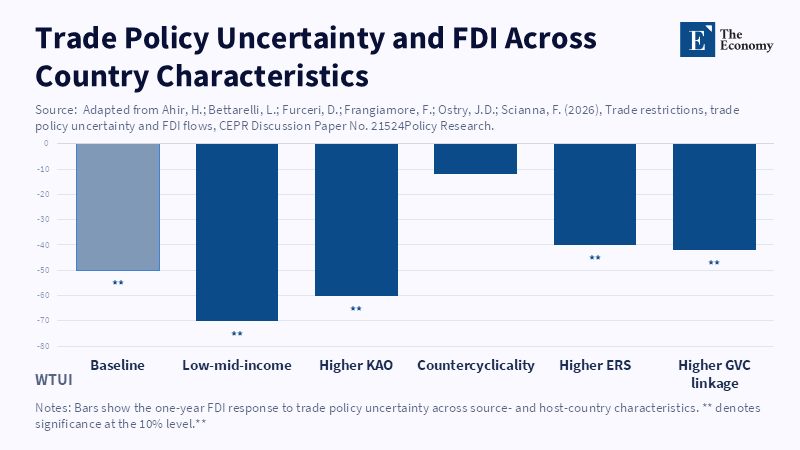

But not all investment links respond equally. The most recent cross-country analysis shows that investors from low- and middle-income economies cut back more sharply after trade shocks. They often have higher funding costs and less time to wait out a policy dispute. Deep links to global value chains tend to magnify the damage that arises, since one new barrier hits many processes all at once. The openness of a host country's capital account tends to speed up the retreat, as firms are better able to shift funds out on higher-risk days-a kind of covert redistributional cost. Trade policy uncertainty causes not only a lower amount of FDI. It can lead the remaining set of FDI inflows to consist of a handful of large foreign firms from high-Income countries, squeeze out operational competition and deepen the case for relying more heavily on fewer but larger foreign investors.

Sound macroeconomic policy can also decrease the shock. Countries with stable exchange rates and countercyclical budgets experience less FDI loss after a trade shock. These policies give investors certainty that a trade war will not turn into a currency crisis or a stagflation tax. Political risk insurance can mitigate some specific risks, such as war and asset seizures or restrictions on currency conversion. But insurance alone is only a safety net. A report by the Multilateral Investment Guarantee Agency showed that only a minor and declining proportion of FDI into developing countries was covered by new political-risk coverage. The report also found that 80% of the surveyed agencies expected friend-shoring and near-shoring to benefit their countries. It could benefit their countries. But they cannot all be winners. The future for the winners will combine infrastructure and access with predictable and dependable rules of the game.

A Predictability Test for Every New Trade Rule

All significant trade rules should be subject to a predictability test prior to legislation. The test should ask whether the purpose is transparent, whether the instrument is narrower than the problem and whether the instrument allows rational compliance. It should assess costs throughout the value chain, even for the protected final sector. The test should consider the impact on new projects, incumbent investors, small firms and investors from poor countries. And it should specify what information would cause a rule to be grandfathered or repealed. This is not a plea for policy gridlock. It is a plea to build state capacity. Governments already utilize budget notes for appropriations and impact assessments for major projects. Trade disciplines capable of redirecting billions in durable, long-lived capital ought to require the same degree of deliberation.

Change the sales pitch. Tax holidays and sweet permits are far less attractive when another ministry can poke holes in market access without notice. Agencies should offer a record of policy risks next to their concessions. They could record intimation periods, permit renewal cycles, legal disputes, treaty risks and backdated changes. Investors would have a less fuzzy frame of reference. Governments would suffer more pressure to improve the picture. The broader risks are large. The International Monetary Fund estimates that deep FDI fragmentation along geopolitical lines could reduce global output by about 2% in the long term. It would be the poorer countries and those that rely on outsiders' capital and skill that stood to lose most. Foreseeable rules cannot resolve the types of geopolitical antagonism that undo even the most favorable market shifts, but they can prevent a nation from adding a self-inflicted risk premium.

The opening figure makes a strong preemptive statement. A Brexit-level increase in trade policy uncertainty generated an immediate FDI loss of about 40 percent of the sample mean and a more pronounced loss at the end of the following year. No tax break can easily compensate for a risk so large. No summit on investment can restore confidence with rules that are up in the air. A nearby war can unsettle investors even in a nonbelligerent state. An administration that introduces durable uncertainty accomplishes something even worse: it turns prudence into policy. The solution is not to promise that rules will never change. It is to create a change mode that is lawful, narrow, transparent and reversible. Countries that build discretion into their policy infrastructure will retain more capital when the next shock hits. Countries that use unpredictability as a strategic tool may find that their investors have jumped ship before the barrier take effect.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Advisory – Risk Desk (2026) ‘Top 20 Geopolitical & Political Risk Advisory 2026’, Advisory Ranking.

Ahir, H., Bettarelli, L., Furceri, D., Frangiamore, F., Ostry, J.D. and Scianna, F. (2026a) ‘Trade restrictions, trade policy uncertainty and FDI flows’, CEPR Discussion Paper No. 21524. Paris and London: CEPR Press.

Ahir, H., Bettarelli, L., Furceri, D., Frangiamore, F., Ostry, J.D. and Scianna, F. (2026b) ‘How do trade restrictiveness and trade policy uncertainty affect FDI? An empirical investigation’, Bruegel Working Paper 12/2026. Brussels: Bruegel.

Ahir, H., Bettarelli, L., Furceri, D., Frangiamore, F., Ostry, J.D. and Scianna, F. (2026c) ‘Trade restrictions, trade policy uncertainty and FDI flows’, VoxEU, 18 June.

Ahn, J., Carton, B., Habib, A., Malacrino, D., Muir, D. and Presbitero, A.F. (2023) ‘Geoeconomic fragmentation and foreign direct investment’, in World Economic Outlook: A Rocky Recovery. Washington, DC: International Monetary Fund, pp. 91–114.

Bloom, N. (2009) ‘The impact of uncertainty shocks’, Econometrica, 77(3), pp. 623–685.

Caldara, D., Iacoviello, M., Molligo, P., Prestipino, A. and Raffo, A. (2020) ‘The economic effects of trade policy uncertainty’, Journal of Monetary Economics, 109, pp. 38–59.

European Union Aviation Safety Agency (2026) Airspace of the Middle East and Persian Gulf. Conflict Zone Information Bulletin 2026-03-R12, 10 June. Cologne: EASA.

Ghodsi, M. (2019) How Do Technical Barriers to Trade Affect Foreign Direct Investment? Evidence from Central, East and Southeast Europe. wiiw Working Paper No. 160. Vienna: The Vienna Institute for International Economic Studies.

HNW – Legal and Arbitration Desk (2026) ‘Top 20 Regulatory Defense & Sanctions Boutiques 2026’, HNW Ranking.

Nebe, M., Economou, P. and Abruzzese, L. (2024) Shifting Shores: FDI Relocations and Political Risk. Washington, DC: Multilateral Investment Guarantee Agency, World Bank.

Ranking News Editor (2026) ‘When Cities Compete: How Urban Rankings Influence Global Investment Flows’, The Ranking News, 16 March.

United Nations Conference on Trade and Development (2025) World Investment Report 2025: International Investment in the Digital Economy. Geneva: United Nations.

United Nations Conference on Trade and Development (2026) Global Investment Trends Monitor, No. 50: Global FDI Up 14% in 2025—Growth Limited to Developed Economies. Geneva: United Nations.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.