US-China Tariff War: Why Third-Country Gains Are Uneven

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Tariffs create openings, not automatic winners Europe gains only while it remains outside the tariff wall Productive capacity determines who captures diverted trade

The most striking number from the US–China tariff war is not a tariff rate. It is 80.5 percent. That is the proportion of cross-country variation in export gains explained by one significant paper that plumbs country-specific advantages as opposed to straightforward sector mix. The findings are stark. A trade war distributes benefits neither fairly nor predictably. It opens short windows that only economies with the right firms, skills, finance and logistics can exploit. European high-quality goods may become less expensive than taxed American or Chinese ones. New orders flow into Vietnamese plants. Mexican enterprises enlarge market shares. High-value contracts accrue to Korean shipyards. All of this is neither certain nor universal nor long-term. The US-China tariff war is therefore a test of productive readiness: tariffs create the price gap, while productive capacity determines who captures it.

The US-China Tariff War Reprices the Global Market

The usual story of the US-China tariff war begins with losses on both sides, which place tariffs or export taxes and surcharges in place. That is true, but it is not the whole picture. Between 2018 and 2019, China and the United States elevated duties on $450 billion worth of trade flows. Those higher duties altered relative prices for thousands of products. A producer of Chinese machinery faced with a 25 percent US tariff was not rendered inefficient overnight; instead, it was priced out of the market a little. European, Mexican, or Vietnamese manufacturers were actually priced in the high tariff environment because they sold into a market seemingly outside the main bilateral tariff barrier. It was not merely a movement to lower prices in Europe; it was a movement of prices for one supplier in the direction of another. That advantage can disappear quickly if tariffs change, exchange rates move or the conflict widens.

Early evidence demonstrated the extent of the diversion. During the first half of 2019, US imports of tariffed Chinese goods declined by over 25%. Some of that lost trade was diverted to the other higher-income economies of Taiwan, Mexico, the European Union and Vietnam. Later research identified that the average bystander economy increased exports in tariff-exposed products by 6.5% relative to non -tariffed products. The standard deviation across all the bystander countries was 6.1%, nearly as high. The same pattern appeared among Italian firms, where the average export gain was 2.5%, but that average concealed large gaps between firms. Efficient firms in spheres with strong scale effects gained most, while the less prepared firms gained little or even faced stronger Chinese competition at home in other markets. The overall global image was therefore not one of an efficient transfer of orders but a sorting process that benefited some producers and potentially penalized others.

This reframing of the issue is important because trade diversion is so often conflated with a national 'windfall'. But aggregate export growth can be misleading. You can win by exporting more final goods to one country while losing by exporting less to another. Or you might be exporting more, but you are more dependent on Chinese parts imports. Or you might be creating more jobs in one region, but at a higher cost to downstream firms elsewhere. Counting dollar gains from a model of the 2025 tariff escalation delivers the same warning. European firms can gain temporarily by replacing Chinese goods in the United States and American goods in China. Those gains weaken when global demand falls or tariffs spread to European products. The right question is not which of Europe, Asia, or Latin America will win America's new trade policy? It is what firms will 'win', how long those gains would last and whether their capacity expansion would justify a price gap closure.

Heterogeneity Determines Who Captures the Tariff Gap

Heterogeneity isn't a sideshow. It's the main event. Tariffs impact demand first; actual supply conditions settle what happens next. A country gains when its products are close substitutes for the taxed goods and its firms have spare capacity. It gains less when factories are full, imported inputs are costly, or logistics and standards prevent rapid expansion. Labor also counts: import-competing workers might gain in the short run, but producers of their own inputs might gain less and exporters may have fewer customers or pay higher prices. It could be, say, that the same tariff boosts one factory, depresses another and leaves a third trading in place. What national averages don't show is that this conflict exists.

A look at the US market shows why substitution alone cannot do. China's share of US imports dropped from 21.6 percent in 2017 to 16.3 percent in 2022. In tariffed product lines, US imports from China were 14 percent below their 2017 level and imports of those very same product lines from the rest of the world into the US increased by 48 percent. That appears to be decoupling. But beneath the trade label, a different pattern emerges. Countries that replaced China were often more deeply embedded in Chinese supplies. In strategic sectors, deeper trade links with China were associated with about 4.5 percentage points more export growth to the United States. The dominant trend was not reshoring. It was China plus one: final assembly or additional production built up elsewhere, while Chinese sources stayed within the chain.

Vietnam demonstrates how a tariff opening can deliver a real leap in development. U.S. tariffs on China broadened the spectrum of Vietnamese exports to the American market. Firms that experienced an average tariff differential of over 15 percent saw employment grow by about 5 percent, much of which was predominantly female. This is not an exercise in distortion. It shows that diverted demand can sustain a combination of increased production and employment. But the gain depended on firms that could enter new product lines, meet US standards and connect to established supply chains. Malaysia, Thailand, Poland and Turkey also experienced a bumper period of export expansion in those switched products, though not quite so fast. The policy implication is a complex one. A trade war can hasten the progress of structural change, but only if firms in affected sectors are already of a high enough order. Tariffs alone do not generate that process.

A second manifestation of gain is evident with respect to Mexico. Between 2017 and 2023, the value of Mexican exports to the United States increased by over $160 billion and Chinese imports increased by around $40 billion. Of the latter, about $25 billion were intermediate goods. This points to added production in Mexico, but also to deeper integration with Chinese supply chains rather than a clean break from China. Investment also responded to the transition. Mexico's share of FDI inflows to emerging markets increased from a share of about 6 percent on average in the 2010s to nearly 10 percent by 2023. The strongest effects appeared in northern regions with established manufacturing bases. Central location was an advantage, but the appearance of such a considerable global supply network depended on infrastructure, power, transport, skilled labor and customs.

The Shipbuilding Lesson: Capacity Beats Protection

Shipbuilding provides a striking stress test for the broader argument. Japanese and Korean yards suffered years of squeeze as Chinese capacity grew and prices slumped. The recent order cycle has seen better profitability, more in premium segments and less risk for owners. However, the data dismiss any simple notion that US barriers have returned the old market order. In 2023, China supplied more than half of global new ship capacity for the first time; South Korea supplied 28.2 percent and Japan 14.9 percent. China dominated the majority of segments, South Korea maintained a comparative advantage on liquefied gas carriers and some very complex ships. Japan remained a leader in quality and marine gear and efficient ships, but its otherwise comprehensive market share continued to be under sustained challenge. Protection may redirect some orders. But it cannot wipe out the enormous cost and capacity differential.

The same sector also shows why the same shock has different effects within a single industry. A bulk carrier, an LNG carrier and a naval support vessel are not substitutes. They use different shipyards, engineering talent, safety regulations and supply networks. Korean firms could profit from the demand for LNG carriers since they have already exploited technical advantages. Japanese yards could profit where fuel saving, reliability and home-market planning are concerned. A tariff or port fee directed at Chinese-built ships could increase interest in those alternatives, but in the short term, the supply response is constrained by labor shortages, busy yards and long build times. When yards cannot expand capacity, ship prices rise instead of output. The nominal beneficiary may be the end producer who has the rare slots, but the costs to shipowners and cargo operators increase.

This broader concept of heterogeneity explains why, in a US- China tariff war, the decisive unit is not the country at the aggregated level and not even the sector at the sector-aggregated level. The decisive unit is the production system around a product: parts makers, engineers, certification bodies, ports, banks, insurers and energy supply. Even a famous industrial brand can, because one link is missing, fail to win new demand, or, through narrow specialization, expand in one market while its other markets shrink. Headlines about announced domestic market shares will get these distortions wrong. A more robust procedure is to locate substitution where technically possible, where spare capacity can be activated and where additional demand will generate downward pressures on prices where otherwise bottlenecks would appear. This map must be constantly revised in light of changing prices and order flows.

Turn Tariff Diversion into Durable Productive Capacity

Governments should regard tariff diversion as a temporary opportunity, not as evidence of a successful new industrial strategy. Their first job is to boost industry in sectors where the tariff gap is sufficiently large for genuine product substitution, as with new cars. The second is to enable firms to increase in sectors where expansion can support learning and supplier development, without depending on just one vulnerable component. Third, eliminate practical barriers to turning orders into supply: everything from power grids via port delays and working capital requirements through to testing equipment, customs systems and technical personnel and export insurance. Removing several small constraints at once can matter more than relying on one large subsidy: the point, for example, is not to undertake every opportunity created by the US-China tariff war, but to find opportunities that build on current strengths and provide a foundation for accumulation, investment and higher quality work.

This also addresses the main criticism. It can be said that any effort to stabilize diverted trade will simply be opportunistic and result in the US economy becoming trapped in an unmanageable war. It is a real danger. The answer, however, is that passiveness will also be costly. Some firms are already suffering damaged prices, diverted Chinese exports and depressed demand in some markets. The choice is not 'intervene or watch free trade remain stable'. The choice is between rigidly adjusting and being exposed to unmanageable risks. Support should be conditional. Public money should be awarded for capacity-creating projects, workers being trained, energy consumption reduced, supply sources diversified, domestic content being declared and checked. Public support should be withdrawn when the tariff opening closes or when firms fail to reach targets. Rules of origin and customs checks should prevent cheap transshipment, which causes political problems without developing the local industry.

Europe has a valid argument for being more cautious. Its broader export base enables firms to substitute American products in China and Chinese products in the US. But the same openness leaves European producers more exposed when Chinese supplies are channeled to Europe. A temporary foreign market share gain comes with a risk of tougher competition at home. European policy should thus distinguish three different types of firms. Firms able to capture redirected demand may justify targeted export support. Viable firms threatened by a temporary import surge may need time-limited adjustment support. But some should not qualify for protection at all, since the tariff shock has actually revealed deep-seated problems, not unfairly redirected supply. The test should be the company's inherent marketability and prices over the years ahead, not the political prominence of presenting a case. Retaliation should stay proportionate and be easily reversed, excluding further key inputs, to prevent a costly general inflow of input tariffs into the economy.

The opening statistic points to the final rule. If country-specific advantages account for more than four-fifths of the between-industry dispersion of export benefits, tariffs are not the cause of persistent superiority. They are only the trigger. The tariff war between the United States and China can set up a price differential, but it cannot generate a supplier network, educate welders, fund a new factory, or decongest a port. Those are the steps that determine whether a transitory order takes on the attributes of a durable industry. Decision makers should stop deliberating abstractly about which nations come out on top in a trade skirmish. They should identify which products can achieve scale, which workers will see higher returns, which inputs remain vulnerable and what is likely to transpire after the tariff levy is lifted. The next tariff window will close. The only defensible strategy is to leave behind stronger firms, broader skills and more resilient production than existed when the tariff window opened.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arizala, F., Mineyama, T. and Tuesta, H. (2025) ‘Relocation of global value chains: The role of Mexico’, IMF Working Paper WP/25/180. Washington, DC: International Monetary Fund.

Conteduca, F.P., Errico, M., Leone, F., Panon, L. and Romanini, G. (2026) ‘The impact of trade wars on firms in third countries’, CEPR Discussion Paper No. 21421. Paris and London: Centre for Economic Policy Research.

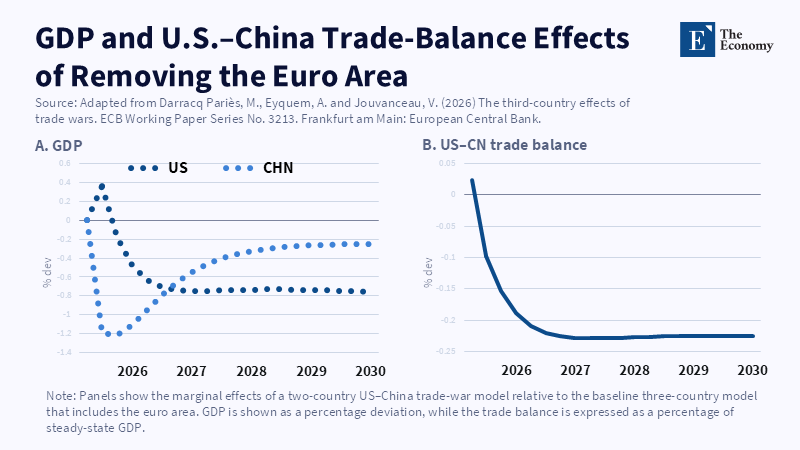

Darracq Pariès, M., Eyquem, A. and Jouvanceau, V. (2026) ‘The third-country effects of trade wars’, ECB Working Paper Series No. 3213. Frankfurt am Main: European Central Bank.

Fajgelbaum, P.D., Goldberg, P.K., Kennedy, P.J., Khandelwal, A.K. and Taglioni, D. (2024) ‘The US-China trade war and global reallocations’, American Economic Review: Insights, 6(2), pp. 295–312.

Fisgin, E., Fleck, J. and Richards, K. (2026a) ‘The design and effect of tariff retaliation: Evidence from the EU’, VoxEU, 17 June. Paris and London: Centre for Economic Policy Research.

Fisgin, E., Fleck, J. and Richards, K. (2026b) ‘The design and effect of tariff retaliation: Evidence from the European Union’, International Finance Discussion Papers No. 1436. Washington, DC: Board of Governors of the Federal Reserve System.

Freund, C., Maliszewska, M. and Constantinescu, C. (2019) ‘How are trade tensions affecting developing countries?’, The Trade Post, 18 March. Washington, DC: World Bank.

Freund, C., Mattoo, A., Mulabdic, A. and Ruta, M. (2024) ‘Is US trade policy reshaping global supply chains?’, Journal of International Economics, 152, 104011.

Lechthaler, W. and Mileva, M. (2018) ‘Who benefits from trade wars?’, Intereconomics, 53(1), pp. 22–26.

Rotunno, L., Roy, S., Sakakibara, A. and Vézina, P.-L. (2024) ‘Trade policy and jobs in Vietnam: The unintended consequences of US-China trade tensions’, IMF Working Paper WP/24/263. Washington, DC: International Monetary Fund.

United Nations Conference on Trade and Development (2024) Review of Maritime Transport 2024: Navigating Maritime Chokepoints. Geneva: United Nations.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.