Japan’s Yen Dependency Trap Is Deepening China Reliance

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Japan’s weak yen is making economic security more expensive Cheap Chinese imports now help Japan contain inflation Only productivity growth can weaken the yen dependency trap

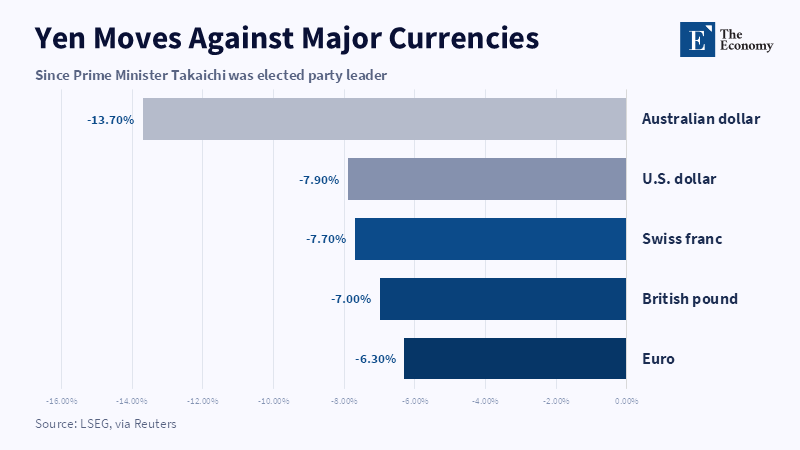

This yen story has a number that explains Japan's economic predicament better than the dozen slogans about security and reform, compromise and sacrifice that go with it: the yen has hovered around 160 to the dollar ever since Japan started propping up its currency to record levels. When that is your exchange rate, everything that is priced in dollars-energy, food, imported technologies-becomes more expensive. But the same weak yen also provides relief to exporters and makes cheap Chinese goods a more effective inflation cushion. That is the yen dependency trap. Japan has a historical desire to extricate itself from China-centric supply chains, but its fiscal and monetary structures are forcing it in the opposite direction. For firms, a weak currency is a blessing. For households it is a nightmare, destroying your purchasing power and raising the cost of reconstruction at the same time. Over the medium and long term,it also weakens Japan’s growth. Economic security cannot be built on slogans while the exchange rate, the debt load, an aging population and sluggish growth all point in the same direction.

The Yen Dependence Trap is not Just a Currency Story

This yen dependency trap is best interpreted as a production problem rather than as a market problem. The market story emerged from the policy forum, many will still subscribe to– that the way to better China relations is for Japan to have less exposure to Chinese direct investment and trade. This is largely right. But the more instructive reality is that how quickly re-risking can occur in a Japanese economy structured like today's is limited by the high cost of separation; firms continue to need cheap supplies; households, cheap consumption; the state to have some inflation without the inflation raising interest bills so high that the domestic public debt burden then becomes an 'unsustainable' burden. And this is precisely where depreciation becomes a bug, not a feature. It pushes up abroad costs, food, commodities and dollar-financed inputs; the intensity of China-scale economies and the leverage that scale now confers, making ruptures less, not more likely.

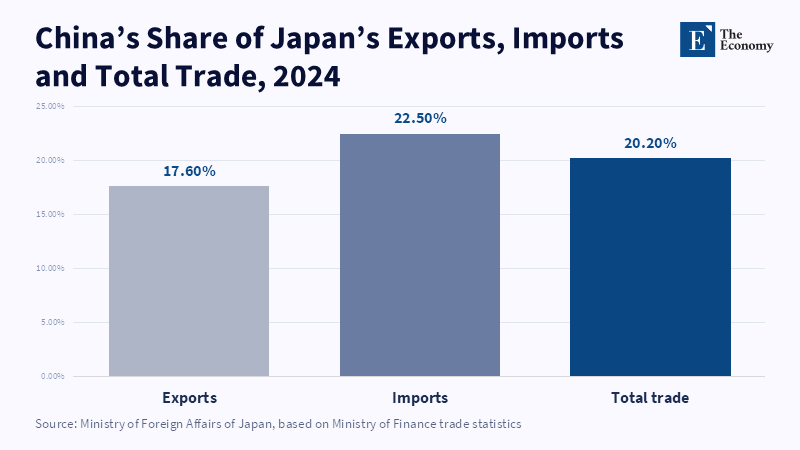

Trade figures reveal why this is a structural problem. In 2024, total Japan-China trade stood at 44.2 trillion yen. The figure accounts for 22.5 percent of Japan's imports and 20.2 percent of Japan's total trade. It wasn't just toys or other rudimentary products that constituted these numbers, but was comprised of computers, telecommunication and clothing goods. As of October 2023, Japan had more than 31,000 overseas bases in China than in any other country. These figures don't imply that Japan should accept dependency as a 'destiny'. They imply that dependence is 'woven into prices, firms, logistics and consumer welfare. Japan cannot unravel this in a handful of years, even under subsidy schemes.

Cheap Imports From China Now Suppress Japan's Inflation Problem

Where the real danger lies of a stagnating economy driven by an inflationary yen is in the number of it. A weak yen affects more than (however important) the Tokyo deal rooms. It translates into the expense of evening meals, means of transport, input costs at the factory and corporate planning. In May 2026, Japan’s producer prices rose 6.3% year over year, while the import price index, measured in yen, increased 25.5%. That is going to be a jolt that makes it very difficult for firms to find other ways to cope other than passing these costs on to consumers, even if consumers don't have the purchasing power to meet all these price increases. It thereby constrains what the Bank of Japan can do. Because while increasing rates will support the yen, it will simultaneously dampen demand and exacerbate debt-bearing costs. Keeping rates well below neutral will do no favors for borrowers, but it could leave another import-led inflation shock off the leash to get another time.

This is why broad decoupling would prove more inflationary than many speeches suggest. Japan can focus on sensitive goods. It can be designed with extra capacity for chips, batteries, rare earth refining, medical supplies and weapons parts. But covering large Chinese flows throughout everyday consumer and industrial parts would push up costs. It would also prove impossible to do overnight. Shipbuilding provides a neat example. Japan remains a serious maritime power, but its leading yard accounted for roughly 11% of world completions in 2024-5, well below historic levels and trailing China and South Korea. As the OECD admits, Japan's yards still have the best quality and engineering, but their costs are held back by wages, buildings and power. The same pattern applies elsewhere. Japan still has many game-changing pluses, but it cannot own its way back into every lost sector.

There is nothing wrong with attempts to de-risk. The question is whether they should be sequenced back into the core architecture. Japan should not mistake resilience for autarky. A more resilient economy is not necessarily one that produces each input domestically. It is one that is aware of which inputs can be vital and which can be supplied by multiple, reliable sources and which imports can remain cheap because they lack any serious strategic threat. With a weak yen, this prioritization becomes that bit more urgent. There is less scope to settle for excesses of waste. Every yen spent subsidizing a low-risk item is a yen not directed towards power grids, ports, personnel, hardware, advanced materials, or military-civilian industrial capacity. The yen dependence trap punishes a lack of clarity.

Debt and demographics deepen the yen dependency trap

Debt and demographics make the yen dependency trap even more risky as they leave less room for policy errors. Japan’s public debt remains well over 200 percent of major international measures of GDP. The IMF projects medium-term potential growth at around 0.5 percent a year. The demography is tight just as much. Japan had 126.15 million residents in 2020. The medium official projection brings this down to 87 million by 2070. The demographic dependency ratio for those over the age of 65 rises from 28.6 percent to 38.7 percent. Such figures are relevant because debt is more easily financed when the working population expands, real wages grow and the tax take increases. Japan is heading the other way.

The weak yen offers a response in the immediate term to some troubled areas in the country's fiscal system. It lifts the yen value of overseas income for exporters and boosts nominal profits for firms engaged in global sales. However, it transfers this pain to households and subsequent years burdened with taxes. Over recent years, real wages have failed to keep pace with prices. Imported food and energy first take preference over lower-income groups. Young workers face the dual burden of rising living costs and future taxation, the key intergenerational challenge. The Yen trap goes further than Hong Kong or China works. It effectively may be bankrolling the older generations' debt burden while exploiting the next generation to buy the technology of tomorrow, but in a weaker environment.

Japan's balance of payments adds another dimension. In 2024, the current account sweetened to 29.3 trillion yen, the highest on comparable data. But the largest component was primary income earned on global securities and direct investment, which totaled 40.2 trillion yen. That sounds healthy. But much of those returns are plowed back into overseas investment rather than repatriated to Japan. In 2025, Japan's net external wealth rose to a record 561.75 trillion yen, but Japan faltered behind Germany and China as the World's largest net creditor. Japanese investors also lifted their holdings of foreign stocks by 2.22 trillion yen in March 2026. These are common, well-behaved flows. Greater profitability abroad draws the requisite capital. But they also explain why the yen does not strengthen, simply because Japan is earning income in the rest of the world.

Productivity is the only real escape route

No such clean monetary solution exists for the yen dependency trap. Currency intervention can curb the panic. Rate hikes can ease the squeeze. But neither can substitute for the absence of a growth model. If Japan maintains a weak yen to aid exports, the problems of import dependence and household pain persist. Too rapid a tightening of policy risks consuming demand and creating fiscal stress. The only sustainable exit is not just productivity growth strong enough to prop up real wages, revenue and a stronger exchange-rate position. It is precisely what weakens Japan. Japan's per-hour labor productivity on a PPP basis was $60.1 in 2024, ranked 28 th among 38 OECD countries, the lowest of the G7 and lowest among all advanced economies. Past OECD calculations also indicate that such measures of per-hour productivity growth were down from 1.2% per year between 2000 and 2008 to 0.3% between 2019 and 2024.

The policy response has to be more targeted than the national revival plan. Japan must stop so complacently treating economic security as if all supply chains are created equal. The state must first delineate sectors in which dependence will cross the line into coercion and then develop targeted capital and talent in those areas. That can include government strategic reserves, trusted suppliers and domestic capacity in a narrow set of strategic layers. But it shouldn’t mean trying to compete with low-cost imported inputs in all other areas, which nonetheless can help buy Japan time, provided it uses that time productively. Those benefits should, in turn, be converted into digital adoption by small firms, capital investment in energy-efficient assets, labor mobility, advanced research and the accelerated exit of low-productivity firms when their capital is trapped. Japan also needs more inward investment and immigration, not only as a way of bolstering the economy in itself but also as a source of comparative scale and new knowledge.

The most difficult reforms are not technical; they are political. Japan cannot keep up its social peace by protecting low-efficiency stability institutions. The goal is not to get rid of every small firm suffering from labor and energy shortages. But weak firms should not be kept alive without a productivity path, not merely to facilitate their survival, since they disperse employees among too many low-yield activities, reducing real wages. Better incentives for merging, investing in digitalization and skills and selling on to stronger firms would be more efficient. The same applies to public finance; subsidy programs would have to command convincing international and domestic benefits: value-added, spillovers, energy savings, supply-chain security, productivity gains and employment creation. Without predefined efficiency demands, economic security is only a high-priced industrial policy.

Critics will say the yen will bounce back as global rate differences shrink-that is true. Coming back from 160 to a more competitive level would remove some of the build-up of pressure. But a cyclical recovery can not be regarded as a structural solution. The old idea that the dollar 'should' be sitting comfortably at 100 yen is no longer a benchmark for policy. Glide down to 200 yen in the coming decade is by no means impossible, even if it is no longer a reckless worst-case scenario if growth is sluggish, capital remains a one-way trader and the cost of living for everyone else stays so high. Another criticism states that the yen is a good thing because it boosts exports. The second half is true-that is only half a good strategy. A currency system that boosts exporters by making oil, grains, chips and foreign software more expensive is not a recipe for increased growth. That's a choice.

Japan is therefore faced with a difficulty more severe than the familiar China policy debate implies. It can keep running the weak yen and cheap Chinese supply to mask the tests of stagnation. Or it can take this agonizing period to do away with the underlying tendency. The second approach will take longer, but it is the only approach supported by the facts. It involves fewer global subsidies and tougher policy compromises. It involves fewer sectors going into bankruptcy and those sectors being protected, well. It involves raising productivity in services rather than only subsidizing famous makers. It involves allowing failure for Weak firms and growth for strong. Most importantly, it involves looking at the yen not as the motor but as the warning light.

The opening number should be the test. If Japan is willing to and able to spend record sums yet still sees the yen hover around 160, then the problem is not just mood. It is the structure behind the market. And the yen dependency trap won't be defeated by telling firms to shift the cost base abroad while retaining the same bundle of inputs. Neither will it be relaxed by denying consumers the returns to prosperity by asking them to bear higher prices. And it definitely won't be alleviated by waiting for the US cycle to turn. Japan's next move in economics must follow just one guideline: strategic independence without productivity gain is easily corruptible dependence.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Fujita, J. (2026) ‘Weak yen, hawkish Fed adds to pressure on BOJ to accelerate hikes’, Reuters, 9 June.

International Monetary Fund (2025) Japan: 2025 Article IV Consultation—Press Release; Staff Report; and Statement by the Executive Director for Japan. Washington, DC: International Monetary Fund.

Japan Productivity Center (2025) Labour Productivity International Comparison 2025. Tokyo: Japan Productivity Center.

Kihara, L. (2026) ‘Japan wholesale inflation accelerates to fastest in 3 years as energy costs spike’, Reuters, 10 June.

Ministry of Foreign Affairs of Japan (2025) China’s Economy Overview: Japan-China Economic Relations. Tokyo: Ministry of Foreign Affairs of Japan.

National Institute of Population and Social Security Research (2023) Population Projections for Japan: 2021 to 2070. Tokyo: National Institute of Population and Social Security Research.

OECD (2026) Peer Review of the Japanese Shipbuilding Industry 2026. Paris: OECD Publishing.

Shirai, S. (2026) ‘Japan’s structural constraints reinforce the yen’s new normal’, East Asia Forum, 9 June.

Tan, T. (2026) ‘Weak yen constrains Japan’s economic security strategy’, East Asia Forum, 13 June.

Yamazaki, M. (2025) ‘Japan runs record current account surplus in 2024 on foreign investment returns’, Reuters, 10 February.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.