The Housing Crisis Is Also a Construction Productivity Crisis

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Construction productivity is holding back housing supply Cheaper machines have not offset rising material and labor costs Housing policy must make building faster, cheaper, and more repeatable

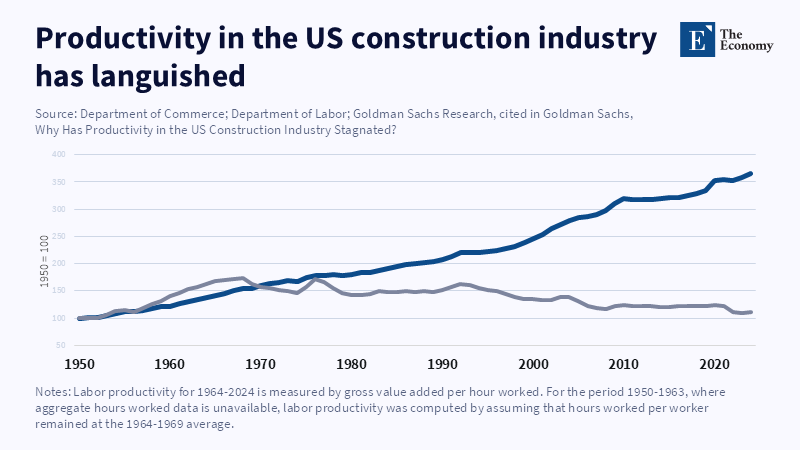

Construction productivity is the missing hinge in the housing debate. U.S. construction labor productivity in 2023 was essentially the same as it was in 1948. In the same span of time, the rest of the economy has become far more productive. That should alter how the barriers are understood. The issue is not just land, permit, or housing demand. It is the modest ability to translate land, labor, materials and regulations into affordable dwellings. Machines are now cheaper, software is smarter and money is quicker. But modern buildings have not fit that model. Advanced economies can produce cheap gadgets, quick logistics and affordable digital services. But they still produce too few affordable houses.

Construction Productivity Is the Core Housing Constraint

Housing policy begins with planning rules. That is understandable, but it is misleading. In addition to broad guidelines where housing will go, such as zoning, appeals, height limits, parking rules and local veto points, the question remains: how will the homes actually get built? Even with an approved project, a developer faces a difficult industry that is hard to manage at scale. Builders work on isolated sites with little margin for error, battling weather, continuous plan revisions and long chains of subcontractors. This is th hidden cost behind every building boom: construction productivity. The barrier explains why more permits do not translate into a proportional increase in housing production. It also explains why property-rich, demand-saturated cities have accumulating urban prices but compressed housing supply. Demand is focused, but delivery continues slowly, locally and in pieces.

The key policy point is fairly straightforward. A housing system must be measured not simply by the number of units it desires but by the number of units it is able to produce, refurbish, or reconfigure at an affordable cost. Over the past 10 years and despite some post-pandemic moderation, OECD averages of real house prices have increased by more than 40 percent. This has not been simply demand-driven. There has been a supply-side constraint also. When productivity in the construction industry is low, a new unit requires the investment of excessive time, labor and risk. Consequently, public subsidies purchase a lesser number of homes, more private projects end in failure and households encounter structural prices that tend to outpace wages.

The macro issues are even more significant than the construction industry. Construction was approximately 4.5 percent of U.S. GDP and 5.2 percent of nonfarm payroll employment in 2024. That means the sluggish output per worker in construction is a matter of national growth not a headache for builders. Studies from the last decade indicate that the productivity of U.S. construction has been declining since the mid-1960s, while productivity in the rest of the economy was increasing. That performance gap is of enormous consequence because the cost-intensive process of building homes, schools, hospitals, factories, transmission lines and transportation networks is common to all of them. When output per worker in construction stalls, the cost of every public initiative increases. Quality standards for the green transition are tougher to meet. Budgets for infrastructure upgrades are eroded in real terms. Pledges to deliver on the housing agenda are weakened even before the first pile of its foundations is driven.

Cheap Machines Cannot Offset Costly Materials and Labor

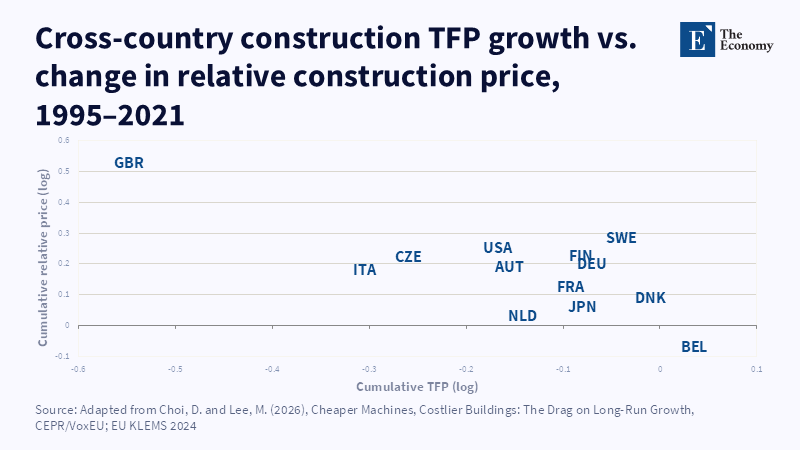

The optimism that better machines would reduce construction costs has not materialized on the relevant scale. Equipment has certainly advanced, but the all-in full cost stack has moved in the opposite direction. Construction prices in the European Union for new residential dwellings surged in 2021, with an acceleration in 2022 and reached high single-digit annual growth rates in most countries. Construction prices increased further in 2023 and 2024, but at a more moderate rate. In the United States, a similar strain in construction materials was observed post-Pandemic. The lesson is not so subtle. A cheaper tool cannot compensate for costlier steel, concrete, wood, insulation, electrical systems, capital, or labor if the project is slow and prone to delays.

Labor exacerbates the bind because construction remains uniformly physical. It needs carpenters, roofers, electricians, plumbers, masons, machine operators, inspectors and site managers. They are largely skilled and potentially hazardous. They compete with other skilled jobs in rich economies and when productivity isn't increasing, wages are a cost shock, not a reward for higher output. This goes some way to explaining the surprisingly large role of migrants. In the U.S., in 2024, they constituted 26.3 percent of construction workers and around one-third of construction trades. Among several larger states, they were close to 40 percent or more. Europe has a similar story. Migrants have helped ease labor shortages and they tend to be overrepresented in construction.

This should not be interpreted as a criticism of migrants. It is a criticism of relying upon migration as a proxy for construction productivity. Migrant workers can keep building sites staffed. They can relieve pressure points. They can sustain growth in the aging population. But they will not compensate for a production regime that requires rapidly mounting labor input in order to deliver each home. Should migration stall, then costs escalate. Should wages be forced upward, then costs escalate again. Should material costs soar, then costs escalate yet again. A sustainable program of housing should be one in which the input of labor and materials is reduced by the incorporation of lean design, streamlined approvals, improved sequencing, enhanced modular automation and more off-site fabrication.

Construction Productivity Fails Where Scale Fails

The most robust reform strategy starts with scale. Whether through greater repetition of jobs, the insulation of fixed costs, the creation of crews, or the reputation effects of experience, productivity improves in manufacturing. Not so in construction. Local regulation channels demand for small projects; opposition to large developments means that every million pounds of capital invested in them is also a risk of many months; builders adapt to this reality through the proliferation of micro-firms competing on one job at a time and not through the platform that evolves and gains efficiencies with each repeat.

This is why these two approaches to land use reform and increased productivity in construction must be considered as one single policy agenda. Upzoning is important but not sufficient. Reform should enable repeated building performance. This means obvious design rules, speedy approval of what conforms, standardized mid-rise typologies, regular inspections and if the block calls for it, some public incentives for modular or panelized constructions. The aspiration should not be that all cities look the same, but that enough legal and technical variation is standardized so companies can learn from practice. A builder practicing one case and at the same time the same job can learn its crews, best prices for supplies, lower errors and reinvest in panelized or off-site mass production techniques. A builder forced to fight a new approval battle on every small project cannot do that.

Japan and Korea encounter this same problem, but from the other side of the market. In the urban cores, with an otherwise high demand but undersupply, builders still compete for dense projects since the final price can take all the market risk. In aging suburbs and rural towns, while vacant homes can indeed exist, they do not necessarily constitute an available supply. Japan's 2023 housing survey registered around 9 million vacant homes, roughly 13.8% of the total housing stock. Many existing homes are located in low-demand areas, weakly inherited, in a poor state, or with high renewal costs. Rural Korea is suffering from a related issue of vacant homes, rooted in aging, migration and declining local markets. A home can be in mapping data and yet not be present in the available housing stock.

The policy response needn't feel sentimental. Not every vacant building can be upgraded economically. Some buildings should be renewed. Others should be rehabilitated. Still others should be knocked down. And some locations simply need land aggregation and consolidation more than a one-time grant. Public administrators must become market makers to encourage the reuse of neglected stock. They can aggregate demand for renovation, set aside initial designs and approvals for standard packages of repair work and create vendor pools. They can delineate blocks of homes where existing renovation potential can be reliably documented. And they can build market confidence. By doing so, a large chunk of historically expensive, often ineffective renovation activity can be converted into a viable production pipeline that firms will be glad to attend to. If not, progress will be spattered by buildings incrementally falling into neglect next to urban shortages. Small vacant inventories, high housing quality deficits.

Physical AI Is Useful Only If the System Is Ready

Physical AI is the most promising solution, but it is not a panacea. Robots that lay bricks, print walls, survey sites, deliver materials, or operate plants can slacken the squeeze on scarce labor. Machine vision can pick up setbacks before they occur. AI scheduling can stamp out unnecessary delays. Digital twins can spot clashes before components are delivered. These are valuable tools and one or two are becoming mainstream. However, they cannot, on their own, add much to construction productivity if they are simply plugged into the existing failed system. A robot does not bypass a permit issue. A drone does not make a complex, fully bespoke design repeatable. A clever program schedule does not fix a flawed supply chain.

The construction technology record of the past decade reads as a cautionary tale. Many new ventures seemed to offer faster sites, cleaner data and lower costs. Various technologies helped in design, safety, procurement, or project management. But theaverage site was not transformed into a factory. Much technology proved to be a nicer interface for paperwork rather than a lower-cost information enterprise. This has its reasons. Owners are seeking flexibility. Contractors carry delivery risk. Subcontractors cheapen their narrow profit margins. Government officials are trying to stem their political risks. Neighbors are fighting their disruptive side effects. Each stakeholder may choose a new tool, but the entire system may then continue to underperform. The sweet spot for improving construction productivity is when new technology actually transforms the pattern of work on site, not just the pixel landscape on the screen.

Physical AI should thus be yoked to public demand, training, codes and scale. Governments can make public housing, schools, care homes, Infrastructure maintenance and test beds for repeatable robotic techniques. Large clients can give the companies a steady enough workload to justify investment. Training programs can allow workers to manage the machines, run off-site manufacturing and maintain automated equipment. Housing and building codes can approve factory-made parts as safe without needing every project to go back to the drawing board to reestablish the basics. The intention is not to eliminate a worker entirely. It is to increase the profit per skilled worker, so the wages can increase without making homes less affordable. That is the true measure of construction productivity.

The Policy Choice Is to Build Differently

From the most coveted inner city neighborhoods, that’s true; from those few areas alone, it is not a reason to stop working on construction productivity. Land becomes more expensive when availability is limited and demand is high. Improved construction methods cannot make primary land available, but they can lower the cost, risk and duration of adding density. They can make suburban infill projects more economical. They can reduce the need for unprofitable public housing subsidies. They can render existing buildings more rentable. Without construction productivity, land reform, reformed finance and tenant protection, each will produce fewer homes than they promise.

The housing crisis has been equated to a dearth of land, capital and political will. It is likewise a deficit of capacity to produce. This distinction is important. A nation that can authorize homes but cannot produce them efficiently has not solved the supply. A nation with an excess of vacant units that are too expensive to retrofit has not solved the vacancy. A nation that depends on migrant workers to reduce site costs has not improved productivity. What must be emphasized in these words is a state of affairs in which the building process is reconfigured. Planning adjustments should unlock a type of density that can be duplicated. Public buying power can be harnessed so as to stimulate stability of demand. Initiatives to retrofit should combine adjacent jobs. Machine intelligence in proximity to standards, training and scale. If the efficiency of a building can remain consistent over multiple generations, it can be altered by design. Policy for housing needs to start there.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Choi, D. and Lee, M. (2026) ‘Cheaper Machines, Costlier Buildings: The Drag on Long-Run Growth’, VoxEU, Centre for Economic Policy Research, 2 June.

D’Amico, L., Glaeser, E.L., Gyourko, J., Kerr, W.R. and Ponzetto, G.A.M. (2024) ‘Why Has Construction Productivity Stagnated? The Role of Land-Use Regulation’, NBER Working Paper No. 33188. Cambridge, MA: National Bureau of Economic Research.

Eurostat (2025) ‘Construction Producer Price and Construction Cost Indices Overview’, Statistics Explained. Luxembourg: Eurostat.

Garcia, D. and Molloy, R. (2025) ‘Reexamining Lackluster Productivity Growth in Construction’, Finance and Economics Discussion Series No. 2023-052r1. Washington, DC: Board of Governors of the Federal Reserve System.

Goldman Sachs Research (2026) ‘Why Has Productivity in the US Construction Industry Stagnated?’, Goldman Sachs Insights, 12 February.

Goolsbee, A. and Syverson, C. (2023) ‘The Strange and Awful Path of Productivity in the U.S. Construction Sector’, NBER Working Paper No. 30845. Cambridge, MA: National Bureau of Economic Research.

International Federation of Robotics (2024) World Robotics 2024: Service Robots. Frankfurt: International Federation of Robotics.

OECD (2026) ‘Housing’. Paris: Organisation for Economic Co-operation and Development.

Shin, S. (2024) ‘Assessing Negative Externalities of Rural Abandoned Houses Using Choice Experiments’, Sustainability, 16(24), 10877.

Siniavskaia, N. (2026) ‘The States and Construction Trades Most Reliant on Immigrant Workers’, Eye on Housing, National Association of Home Builders, 10 April.

Statistics Bureau of Japan (2024) 2023 Housing and Land Survey. Tokyo: Ministry of Internal Affairs and Communications.

Yeh, C. (2025) ‘Five Decades of Decline: U.S. Construction Sector Productivity’, Economic Brief No. 25-31. Richmond, VA: Federal Reserve Bank of Richmond.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.