The Gulf Oil Shock Is No Longer a One-Way Transfer

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

The Gulf oil shock is no longer only an energy-price shock Low-income workers feel the first damage through earnings and job-finding losses Gulf economies now face a deeper test of fiscal strength, investor trust, and capital stability

In 2024, a single oil route carried the equivalent of 20 million barrels of oil a day. That accounted for roughly 20 percent of the world's use of petroleum liquids and over 25 percent of international oil trade. It also provided roughly 20 percent of the total liquefied natural gas trade. That is why one cannot interpret the Gulf oil shock strictly from the perspective of countries subsidizing oil use and generating the oil profits. The old world map is wrong. The shock now hits the seller as well as the buyer. It hits the salaried employee in Europe, the fuel spender in Asia, the willing consumer in Riyadh, the fund manager in Abu Dhabi and the real estate agent in Dubai. The first consequence is energy. The second is confidence. The third, capital. The greatest threat to economic policy is focusing on only the former and overlooking both of the latter.

The Gulf Oil Shock Is a Balance-Sheet Shock Too

The present Gulf oil shock requires a more sophisticated frame. It is not just an external supply shock driving up fuel prices and eroding real incomes in the richest countries. It is also a balance sheet shock within the Gulf itself. The Gulf still sells oil and gas, but they now also sell security, round logistics, wealth services, tourism, real estate and the guarantee that capital can dwell there without bringing the risk of imminent loss. With the erosion of that guarantee, not only will the Gulf producers forfeit their cargo revenues, but also the chance of a safe-haven psychic premium that transformed the Gulf into a platform for global asset accumulation. That premium is badly estimated, but easily lost. It is intricately wired to confidence, not just barrels.

This matters because the financial crisis is hitting a much larger regional economy than past wars. The directly affected economies- Iran, the Gulf states, Iraq, Lebanon and Israel - are worth almost $4 trillion in nominal GDP. That is roughly 70 percent of the Middle East North Africa economy and close to 3 percent of the world economy. This is not a local border shock; it is a stress test for an entire regional growth model. In the 1970s, oil exporters were capitalizing on the scarcity of oil. In 2026, some exporters were experiencing high prices, lost volumes, strained transit routes and higher security costs simultaneously. The advantage gained from pricing power is being eroded by uncertainty.

And the plain truth is this. An oil shock previously directed the flux of wealth to the Gulf. A Gulf oil shock can now lock in wealth within a region that has to consume ever more to compete on the collective routes that render its heretofore liquid assets so. Falling exports erode fiscal earnings despite buoyant spot prices: rising shipping insurance raises net margins despite high spot prices; more rapid Asian and European diversification erodes aggregate pricing influence; the convergence of Abu Dhabi, Dubai, Riyadh and Doha into a bastion of shared security risks alienates the Gulf non-oil engine, too. The policy dilemma is no longer just about how importers combat inflation. It is about how oil states escape an energy shock, which becomes a capital shock to follow.

The Gulf Oil Shock Is Moving from Cargo to Capital

The first is physical. The current energy-shock estimate suggests that the world is missing about 11 mb/d of crude, about 11 percent of world supply, compared to the roughly 20 mb/d of that would have typically flowed through Hormuz prior to the conflict. Market reports did later suggest the stricken Middle East output would be closer to 14 mb/d, about 14 percent of world consumption. Even on the current ceasefire path, full recovery is not instantaneous. Fields might in fact restart faster than refineries-damaged petrochemical and refinery sites take longer to repair-and LNG trains will require painstaking prioritization, but inventories are built up over years. The shock, therefore, persists not only in prices, stocks and contracts, but also in long after first headlines pass.

The second signal is tactical. The UAE's departure from OPEC + and OPEC in May 2026 underlines that Gulf producers are no longer acting as a single, neat bloc. The departure at least opens up room for the UAE to boost output in response to a recovery in flows. Moreover, it undercuts the old "single Gulf commitment" concept that a coordinated and unified supply discipline sustained the commodities rally. All producers have incentives to want to push volumes higher. They need the cash. They need to cover deficits. They need "to protect market share, before locations lock in new long-term agreements elsewhere". More production may boost cash flow now, but it will likely lower margins later. A race for volume is not the same as a race for strength.

The third signal is financial. The UAE has benefited from the war at its most favorable leverage point. In 2025, it was still forecast that the UAE would be receiving a record net inflow (net of outflows) of 9,800 relocating millionaires, while Saudi Arabia would still be receiving 2,400. This does not imply that the wealthy are planning to leave the Gulf all at once, but that the next marginal decision may shift. A family office will keep running in Dubai, but will adopt Singapore. A fund will keep shooting for Abu Dhabi, but be prepared to increase the hurdle rate. A founder might still buy property, but no longer take it as the single regional hedge. The tragedy is not flight, it is retreating to diversification away from total reliance-that takes longer but ultimately can be more permanent.

That can be a problem because Gulf funds are not marginal players. Middle East sovereign wealth fund assets stood at about $4.9 trillion in 2024. Gulf SWFs influence global technology, infrastructure, private equity, real estate and sport. They wield their influence through patient capital, but patience is a condition on fiscal comfort at home. If governments have to deploy larger reserves, borrow more, or lean on their funds to support deficits and security costs, then overseas investment is likely to slow down and become more politicized. The global market would effectively lose a sizeable purchaser as risk premia escalates. This way, an oil shock turns into a financial shock. The channel runs from ports to budgets, from budgets to funds and from funds to global asset prices.

The Gulf Oil Shock Hits Weak Labor Markets First

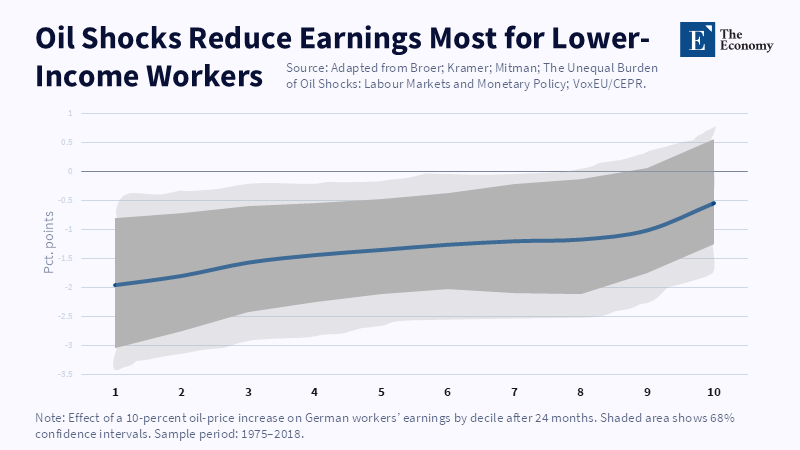

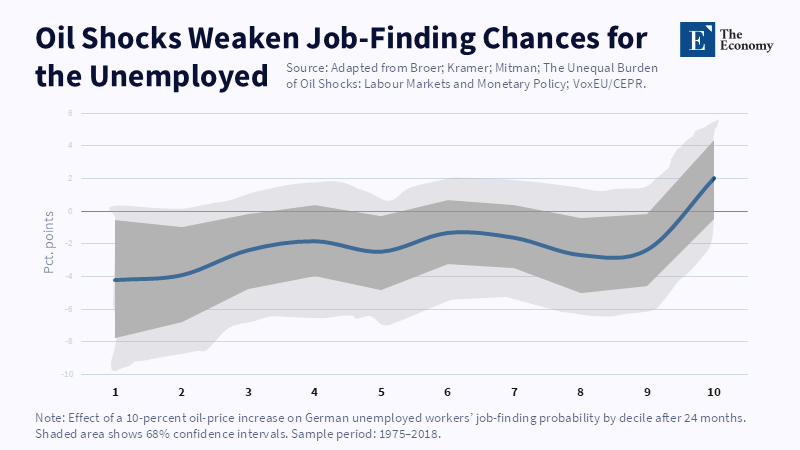

And the labor-market channel still matters most for developed nations. Recall that evidence from half a century of German workers shows that a 10 percent rise in the price of oil can cut bottom-decile earnings by roughly two percentage points 2 years out. Probabilities of finding a job for poorer workers drop roughly four percentage points. The top decile is impacted far less. And it is important that this pattern happened after years of inflation pressure, high interest rates and relatively weak real wage growth in many economies. Those least able to bear higher transport, food and energy costs are those most affected by job loss. The oil bill becomes a labor-market bill.

That is why even the narrow paths for central banks are a trap. Ignoring oil inflation is dangerous because second-round effects will crawl into wages, freight, food and services. Overdoing is deadly too because interest rate rises will crush unprofitable and fragile workers and firms long before they can restore oil supply. So no policy freeze, but separation of instruments. Use monetary policy to defend inflation expectations, of course. Use a targeted, temporary and automatic fiscal injection to shield the bottom of the labor market. Use energy policy to curb demand fast where it can. Never a broad fuel subsidy: they are expensive, blunt and maintain demand. Worse, they trigger exactly the wrong incentives.

For Gulf economies, the labor risk appears quite different. However, it is equally severe. Revenue from oil is used to pay for public service wages, boom and bust construction trends, service jobs and large projects. However, non-oil growth is genuine, but it continues to be heavily dependent on fiscal expenditure, state purchasing power, state-backed credit lines and state-generated confidence. A very recent fiscal study of the Gulf's multipliers shows that the effects of fiscal spending mitigate downturns; however, the multiplier is often below one and consumers of the additional deficit don't always receive the benefit of an offsetting dollar of output. The missing sum is not simply fiscal: it is developmental.

The critique is clear. Oil-exporting countries can draw on reserves, sovereign funds, lax taxation and flexible consumption. Indeed, this is true. But it is also flawed. Resilience does not imply insulation. Saudi Arabia's first-quarter 2026 budget saw oil income fall by 3 percent, even as expenditures increased by 20 percent. It showed a deficit of SR126 billion ($33.6 billion) in that quarter. It did so despite promising signs of a buoyant non-oil sector. Which distorted the message, rather than mitigated it. The region can borrow and leverage reserves. But the successive decades of drawing on buffers for unproductive security costs shift the growth target. It sustains a large state and an idling private sector. And that, it turns out, limits the incoming blow.

A Better Policy Map for the Gulf Oil Shock

The first step to the policy map is a hard dividing line. Energy price relief is not energy security. The correct response for the importers is not panic buying nor permanent subsidy but demand-destabilizing speeded-up demand flexibility. Europe and Asia should boost storage, diversify LNG contracts, build grid capacity, accelerate efficiency and shelter low-income consumers through direct transfers, while shielding against a run-up in consumers' bills from a hard move away from the energy transition once prices have risen. The latest long-range oil forecasts have a plateau of the world's oil demand at around 105.5 mbd by 2030, with electric cars and fuel switching displacing millions of b/d - this is no longer a climate policy but a security one.

As far as the Gulf governments are concerned, the same shock requires a different discipline. Security expenditure may be unavoidable. Yet it must not become a new black hole for oil revenues. Defense budgets need to be balanced by a public test: does this expenditure help to develop some local capacity, or does it simply import mind-boggling hardware? Recent statistics on military expenditures estimate world military expenditure in 2024 at $2.718tn, the Middle East at around $243bn and Saudi-Arabia at around $80.3bn. Stocks of more and more arms may act to safeguard assets, but they will not in any way develop export sectors, better-equipped firms, or enhance taxation over a wider population. Gulf requires security, but also security spending, which does not jeopardize the non-oil economy.

The Gulf Oil Shock Is Now a Confidence Test

The more difficult challenge is to maintain the Gulf's credibility as a capital cushion. That is, not to allow those sovereign boxes to be turned on a short-term basis in support of fiscal shortfalls; to issue more transparent guidelines on the circumstances under which intervention is justified; to ensure borrowings are used prudently-so that the large contingent liabilities in state enterprises do not turn into a future shock; and, to be prepared to persuade both funders and investors that the Gulf is not only rich but also institutionally stable. Capital is more risk-accepting than it once was. It resents non-transparent procedures. The Gulf's oil shock will test laws and credit policies and the fanfare of public communication, as much as the pipelines. Confidence is part of the energy mix.

Finally, the global policymakers must stop treating Gulf fiscal stress as an insignificant side issue in the global economy. In practice, a handful of Gulf investment funds slow down investment and the private market suffers. A handful of Gulf governments minimize spending on projects and the flow of migrant labor is at risk. To restore demand in Asia and Europe, they cut the oil price, which puts stress on a selection of producers. To build up armaments, they increase spending, which pushes up arms markets but reduces civilian expenditure multipliers. A recent downward scenario illustrates how energy- and finance-driven downdrafts weaken each other and drag world demand below the baseline level. And this is the threat. The world economy will not be still. It will not only suffer from costly energy; it will also be weakened by the related loss of confidence.

Meanwhile, the 1970s made oil exporters look like the winners of the oil shocks. But that image now feeds wrong policy: the Gulf oil shock of 2026 reveals a less durable system in which oil producers may simultaneously face high prices and diminishing net power, sacrificing both a buyer and a barrel; hosting foreign capital yet losing credibility as an investment destination; pumping out dollars while weakening the case for using that capital productively and spending on arms at the cost of the very long-term prospects that deployment was supposed to bolster. Not just fear-mongering, but early response remains the best response: import-dependent economies must safeguard the workforce by reducing demand, while Gulf producers must defend credibility beyond the export route; the next oil shock will favor economies that treat energy, workers and capital as one system.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Broer, T., Kramer, J.V. and Mitman, K. (2025) ‘The distributional effects of oil shocks’, IMF Economic Review, 73(3), pp. 851–889.

Broer, T., Kramer, J.V. and Mitman, K. (2026) ‘The unequal burden of oil shocks: Labour markets and monetary policy’, VoxEU, Centre for Economic Policy Research, 12 June.

El Dahan, M. (2026) ‘UAE leaves OPEC in blow to global oil producers’ group’, Reuters, 28 April.

Gross, S. (2026) ‘The Iran conflict’s energy shocks are not yet fully realized’, Brookings Institution, 1 April.

Henley & Partners (2025) Henley Private Wealth Migration Report 2025. London: Henley & Partners.

International Energy Agency (2025) Oil 2025: Analysis and Forecast to 2030. Paris: International Energy Agency.

Liang, X., Tian, N., Lopes da Silva, D., Scarazzato, L., Karim, Z. and Guiberteau Ricard, J. (2025) Trends in World Military Expenditure, 2024. Stockholm: Stockholm International Peace Research Institute.

Salha, A.S. (2026) ‘Iran war poses Middle East’s biggest economic shock in five decades’, Arab News, 11 June.

Shalal, A. (2026) ‘World Bank cuts global growth outlook to 2.5%, warns of drop to 1.3% if war fallout spreads to markets’, Reuters, 11 June.

U.S. Energy Information Administration (2025) ‘Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint’, Today in Energy, 16 June.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.