Europe’s Savings Paradox: Why Abundance Is Not Productive Risk Capital

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Europe has savings, but not enough productive risk capital Fragmented markets keep too much capital in safe, local channels Post-Brexit Europe still lacks a financial centre strong enough to rival New York

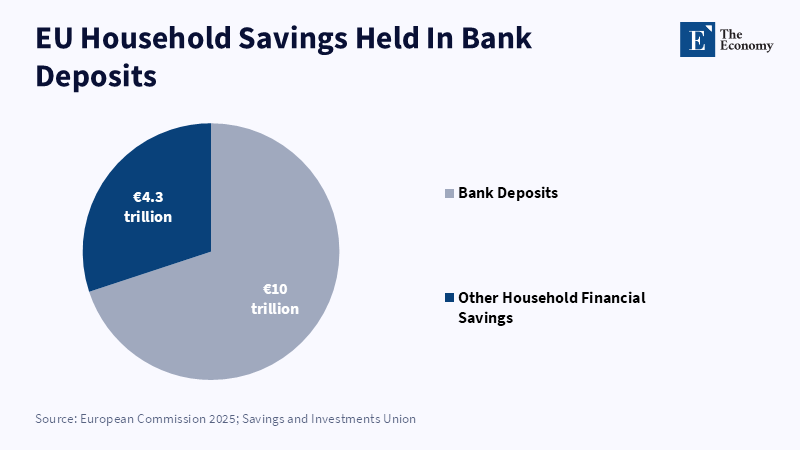

The 70% of household savings accumulated in European Union banks that total €10 trillion alone should surely change the entire debate. It is not that Europe doesn't have enough savings. It is because it doesn't have enough conversion. Europeans save money every day. European insurers are large. European pension funds abound. European control vast portfolios. But not enough of that wealth turns itself into actual risk capital for companies in need of equity, trying to expand, deep capital markets and a viable route between invention and scale. The problem is not a moral problem of careful savers or insecure institutions. It is a design problem. European architecture has opted for a system that protects capital better than it stimulates growth. That old decision was the best one in the midst of the Cold War, state-driven energy transition, artificial intelligence, one of the most sophisticated manufacturing setups known to man and fiscal stress. It's just a strategic bottleneck.

Productive Risk Capital Is Europe's Missing Link

The strongest way to interpret the savings paradox in Europe is not as a tale of too little saving, but too much protection. Deposits provide insurance against loss. Bonds provide a hedge to the insurer against unpredictable liabilities. Banks provide finance to home buyers and comfortable companies. They are relevant channels and an honest reform should aim to preserve them. But they are weak channels for productive risk capital. They do not do the job of funding narrowly defined young firms, with few assets, high fixed costs and little collateral, uncertain scale. They do not do the job of funding sectors in which many of the economic indicators of value are code, data, patents, talent and speed. A bank can lend in the form of collateral. But it cannot lend in the form of a long trial-burn-scale cycle.

That difference is important because Europe's financial needs for sustained investment have shown up within a much slower evolution of its financial behavior. The continent seeks rearmament, decarbonization, a new clean industry, preserving the semiconductor industry, developing strategic AI, while trying to keep more strategic capacity at home. These ambitions are all calling for public financing, but not just that, for additional sources of risk-bearing private finance that will be able to absorb failure while still investing in the very few firms that grow gigantic. A financial architecture that first and foremost transforms household savings into safe assets while secondarily reallocates them into productive risk-bearing infrastructures will fall short of this task. It might remain as resilient as before and fairly well maintained. However, it will continue to require a reliable scope for the public purse to substitute the market.

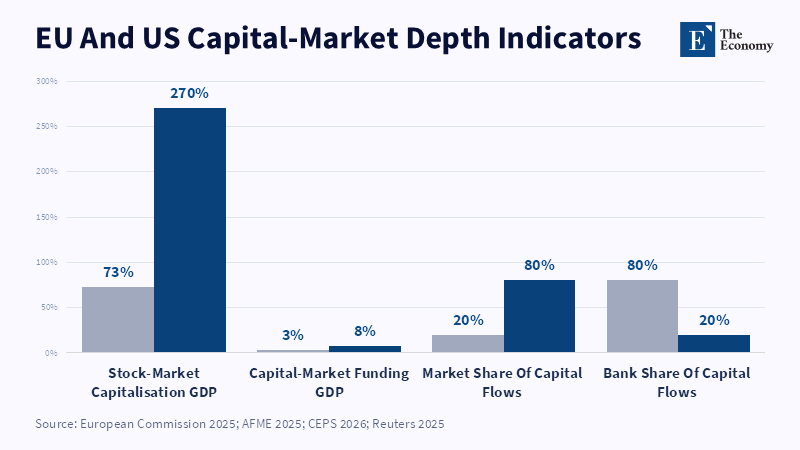

The figures display the extent of the failure to align. Europe's assets under management amounted to some €33 trillion in 2024, with a forecast of exceeding €34 trillion by the third quarter of 2025, according to estimates. By the end of 2024, Europe's occupational pension institutions had some €2.69 trillion invested. These are large sums. But Europe's public markets and venture capital channels remain shallow relative to the US. EU stock-market capitalization in 2024 was given at 73 percent of EU GDP, against 270 percent of the US in 2024; EU firms drew just 13 percent of their funding from market channels in 2025. The problem rests on more than size: it is on what size is allowed to grow.

Why Safe Portfolios Are Rational, Not Timid

It is a comfort to blame the managers. That is too comfortable. European institutions often act more in accordance with peace of mind because the rules, clients and markets they are facing discourage it. The insurers must stress liabilities. The pension funds must stress their members. The retail investors must stress safety. The supervisors must stress solvency. Under these circumstances, sovereign bonds and high-rated corporate bonds are not just conservative choices. They are legible choices. They are an easy explanation for the supervisors. Trustees and the clients. The productive risk capital is difficult to defend because its gains do not offset its losses.

And this is where the charge of risk aversion sounds glib at best. Many European investors accept specific risks. It's just that many of the European risks common today are yield-chasing risks being taken in the US, in global mandates, or in foreign markets. Many European occupational plans had high equity weightings in US stocks during the last reporting period. This does not mean that they were insulated from risks; it merely means that Europe has plenty of risks elsewhere. Home markets simply do not integrate with the rest of the world often enough-they don't have the depth, the negative market depth, exit routes, analyst coverage and late-stage investors. The issue is not only debt versus equity. It's European productive risk capital to the rest of the world's productive risk capital.

That presents a valid counterargument. Prudence is worth it. Europe is older than many rival regions Its welfare systems rely on the trust of actors. A panicked reallocation of too large a share of capital from traditional safe portfolios into unpredictable private markets would be poor policy. It would threaten household finances with unanticipated losses and undermine confidence in retirement schemes. But the opposite risk exists as well. If each of the many institutions of a continent acts prudently in a very narrow sense, the whole will still underinvest. A continent can steer clear of bubbles and still stagnate. The question is not whether safety matters, but whether it must dominate it to such an extent that its stock of future growth drags.

Better policy means altering incentives before it tries to educate investors. Additional funded pensions should be expanded where they are still underdeveloped. The design of retail investment accounts should be straightforward, low-cost and tax-efficient. Savers should not be required to learn it all themselves before they can have a diversified exposure to equities over the long run. Prudential rules should be examined for implicit biases in the favors shown to safe sovereigns, rather than diversified productive assets. But none of this implies a push by policy on households to risk-charged products. It is simply empowering households and institutions to reliably access risk capital into productive activities, with rules, transparent fees and long timeframes.

Fragmented Markets Turn Savings Into Local Pools

The second failure is not cultural. It is geographical and legal: Europe has one market in theory, multiple markets in day-to-day life. Different tax regimes, different insolvency regimes, different listing norms, different regulators, different settlement systems. Funds can be sold across borders, but at scale, cross-border trade is blocked by national friction. Growing firms can expand across Europe, but not as easily as American firms can grow pan-American. And this matters for finance since capital is scale-sensitive. A firm that can reach one large market overnight should be valued quite differently from a firm that has to cross many borders.

Fragmentation erodes productive risk capital in a number of ways. It constrains the universe of analogous firms for which analysts provide coverage. It constrains the universe of analogous stocks with broad-based liquidity. It constrains the universe of analogous stocks with high-quality listings. It reduces the probability that a late-stage investor encounters a suitable exit. And it keeps institutional investors close to their home markets. Insurers and pension funds may want to assemble large portfolios, but still play the role of a national investor. That creates a savings box, instead of a growth engine. The box is full, but it does not push capital enough across the continent. That explains why Europe can enjoy having large financial firms, but underdeveloped capital-market depth.

This is what the 2025 market figures show. In the EU, the aggregate private and public capital-market financing remains at around 3 percent of GDP, while it is around 8 percent in the US. For the EU, after a 23 percent drop in IPOs in 2025, in a few other Large Markets, the IPO volume increased in 2025. Though private markets are growing and are favorable, they cannot substitute the public markets. Public markets provide prices, exits and signals. They transform private investment into a broader story around the market. When that phenomenon weakens, late-stage investors need to be more cautious. And the effect then trickles down to earlier-stage ventures.

The policy lesson is blunt. Capital Markets Union cannot remain a slogan. It must be a more concrete and comprehensive measure. Europe needs to bridge the gaps that have already opened up in insolvency, withholding tax, listing rules, supervision and the post-trade infrastructure. And it needs to complement the current service-driven perspective on market fragmentation with a more coherent definition of what market depth is meant to achieve. This is not about finance for finance's sake. It is about industrial policy through the design of markets. A deeper market will not autimatically lead to more innovation. But a fragmented one guarantees that a lot of firms will either stay small or sell early.

The Post-Brexit Centre Problem Is Still Unsolved

Brexit didn't wipe out London's role in European finance. Claims that Brexit erased London’s role are simply wrong. London remains one of the world’s top financial centres - claims to the contrary are weak. The more difficult point is different. Europe had the old semi-solution whereby its most advanced cluster of finance sat within the bosom of the single market. Activity has shifted to Dublin, Paris, Frankfurt, Luxembourg, Amsterdam and other hubs. Over 440 firms had moved or intended to move some of their activity, staff, assets, or legal entities from the UK to the EU in one major 'post-Brexit' evaluation. Dispersion rather than a new center has been achieved.

Perhaps, this dispersion is possible for compliance. It is a weaker instrument for price discovery. Deep equity finance requires density. It requires bankers, analysts, lawyers, investors, the media, entrepreneurs and multiple repeat transactions within a single power city. A network of specialized markets can perform many functions. But it does not easily generate the same market incentives on supply and demand as New York. The issue is not necessarily: every European financial function should relocate to a single city! That is both unrealistic and impractical. Rather, the issue is: Europe has effectively tolerated polycentric finance. But it has not constructed the common rules and common liquidity that would allow polycentric finance to function as one market.

The listing problem indicates the costs. When large, global technology players locate in New York, it is not only about a flag. It is about a pool of liquidity, valuations, analyst coverage and investor interest. Some European champions are so anchored on European exchanges that they list on US markets as well. This 'double' access may be optimal for the firm. For Europe, it is a warning signal. If its most ambitious firms remain so anchored on a US platform to tap the only deep pool of risk capital, Europe's financial autonomy remains incomplete. Productive risk capital is not only a matter of the origins of savings. It also matters where risks are priced, where firms grow larger and where ownership accrues.

This raises the other side of how policy should decide success. The tests are no longer "where do more firms choose to locate their new office: in one European hub rather than another?" but "where in Europe can a founder in Lisbon, Milan, Warsaw or Tallinn raise larger rounds, list on deep markets and remain European without settling for a weaker chance of scale". This is the practical implication of financial integration, which must be experienced by firms before it is recognized in speeches.

The solution is not to replicate Wall Street. Europe cannot afford to create a financial market that loses sight of consumer protection, financial stability and social trust. At the same time, it must stop dividing safety from scale. Sound systems can still have large allocations to equity. Pension systems can still serve members well by investing for the long term. A supervisor can still prevent insolvency without having to direct surplus capital to traditional assets. The political choice is to normalize productive risk. This can only happen through pension reforms, retail investment channels, larger growth-equity and venture funds, public-market reforms and a much more integrated single market.

The headline figure thus needs to be read less as a household number than as a warning about power. €10trn of deposits is a huge amount of choice for Europe. It can continue to regard savings as something to store, or it can create the trusted institutions that convert some of that store into the risk capital that makes investment a gamble on the future rather than a guarantee of the present. Europe does not have to gamble its savings. It only needs to stop wasting its strategic power.

This article is based on an original research article published by The Economy Research. For the original version, please refer to Europe’s Savings Paradox: Capital Size, Weak Allocation, And The Post-Brexit Financial Centre Problem.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Advisory - Capital Market Desk (2026) ‘Top 20 Capital Markets Advisory 2026’, Advisory Ranking.

AlGarhi, A. and Oyebowale, A.Y. (2026) ‘How Brexit reduced the City of London’s financial clout – new research’, The Conversation.

De Graaf, J. (2025) ‘Passive by default: is euro credit sleepwalking through a shifting landscape?’, Van Lanschot Kempen Investment Management.

Demski, J., McCauley, R.N. and McGuire, P. (2022) ‘London as a financial centre since Brexit: evidence from the 2022 BIS Triennial Survey’, BIS Bulletin, No. 65. Basel: Bank for International Settlements.

Douch, M., Wu, Y. and Gao, B. (2025) ‘How has Brexit affected UK financial services?’, Economics Observatory.

Healthcare - Pharmaceutical Desk (2026) ‘Top 20 Biomanufacturing & CDMO Providers 2026’, Healthcare Ranking.

HNW - Private Wealth Desk (2024) ‘Top 30 Boutique Asset Managers for Private Wealth 2024’, HNW Ranking.

Lappe, M.-S. and Pinkus, D. (2026) ‘Size versus allocation in capital market development: evidence from pension funds and insurance companies’, Bruegel Working Paper. Brussels: Bruegel.

Lavery, S. and Schmid, D. (2018) ‘Will Frankfurt become Europe’s leading financial centre after Brexit?’, SPERI Blog.

Lavery, S., McDaniel, S. and Schmid, D. (2019) ‘Finance fragmented? Frankfurt and Paris as European financial centres after Brexit’, Journal of European Public Policy, 26(10), pp. 1502–1520.

Ranking News Editor (2026) ‘Global ESG Ratings Landscape Expands as New Providers Enter the Market’, The Ranking News.

Thomadakis, A. (2024) ‘Why we need to rewire Europe’s financial sector – to end fragmentation and bolster integration’, Centre for European Policy Studies.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.