Europe’s Savings Paradox: Capital Size, Weak Allocation, And The Post-Brexit Financial Centre Problem

Published

The Economy Research Editorial*

*The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

Europe's financial weakness is often mistaken for a capital shortfall; This article argues instead that the fundamental problem lies in the allocation of capital: The risks of all would-be risk providers are left underfunded in the European system when Europe's high household savings, large asset managers, extensive insurers and pension funds are channeled into deposits, bonds and domestic safe assets. Europe is therefore a high-savings, low-risk capital economy. Conservative institutional behavior is thus neither simply a matter of cultural nor managerial caution; rather it is a consequence of the design of pension systems, household preferences, prudential regimes, growth expectations and the fragmentation of markets. Furthermore, Europe's capital-market weakness should be viewed not primarily as a capital shortfall but as the result of market fragmentation: through supervisory and insolvency regimes, tax codes, listing requirements and the structure of market infrastructure, borders between national markets reduce scale, liquidity and competition. The adverse effects of Brexit are aggravated by the absence of a single centralized EU-integrated financial centre capable of replacing London’s former role inside the single market. f Europe's central political-economy task is therefore to build the institutions, the markets and the growth conditions that make productive risk-taking worthwhile.

1. Introduction - Europe’s Savings Paradox

The recent working paper from Bruegel on pension funds and insurers is usefully macro-directional, even if less analytically illuminating than the policy question would seem to demand.[1] The paper's central contribution lies in its distinction between the size of Europe's capital pool and the allocation of that capital: the issue is not simply that Europe lacks financial resources, but that long-term savings are too often directed toward low-risk assets rather than productive risk capital. The publicly available summary makes clear that the authors separate public-system vs. private-sector size from portfolio structure, suggesting that allocation into a productive set of risk assets matters more for market depth than balance-sheet aggregation.[2] This insight is directionally correct, the more contingent, complex and crucial question is whether Europe's fundamental predicament is merely that its institutions are timid when their American counterparts are bold, or rather that Europe has built an environment that makes caution a rational course of action households keep about 70% of their savings in bank deposits, insurers and pension funds are constrained by their liabilities and prudential capital requirements to favor fixed income, cross-border financial markets across borders are hampered by regulatory barriers and Brexit has left Europe without the single, densely networked deep price-setting core of capital markets with unfettered access to EU internal markets.[3]

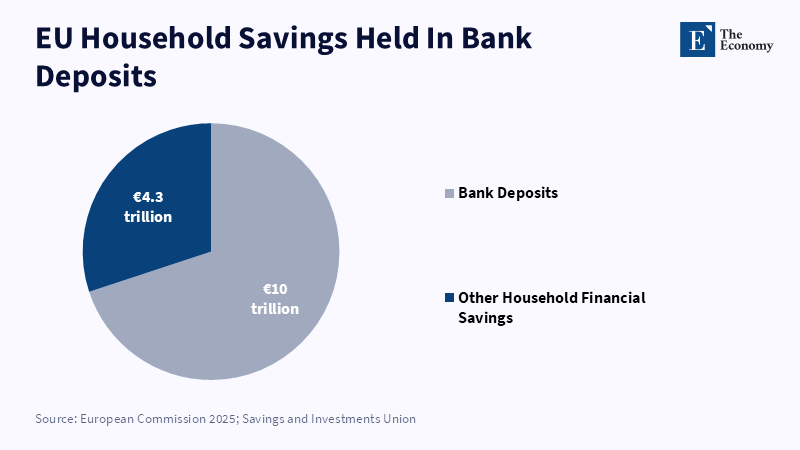

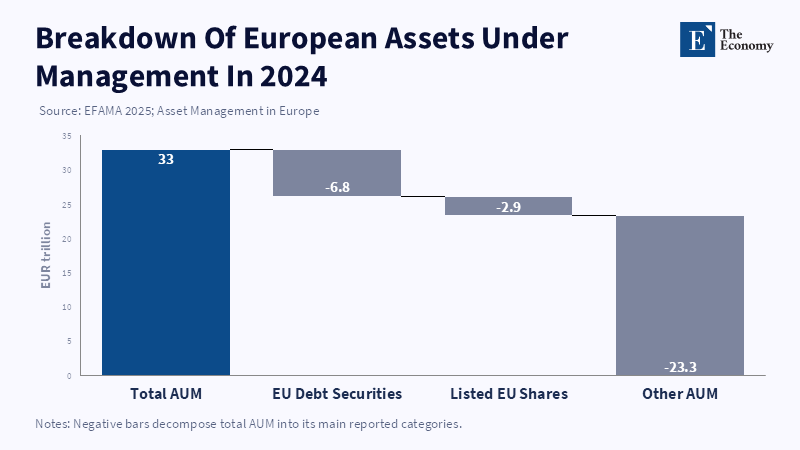

This reframing matters because the most common diagnosis of Europe's financial weakness remains narrowly defined. One version argues that Europe simply needs more capital markets. Another version claims the continent has plenty of savings and that the real problem is a lack of institutional daring. Both assertions are correct, but neither explains the potential mechanism. Europe does indeed have very large levels of pools of savings. In 2025, the European Commission reported that about 70% of EU household savings, roughly €10 trillion, were held in bank deposits,[4] while EFAMA estimated European assets under management at €33 trillion in 2024 and €34.4 trillion by the third quarter of 2025.[5] Thus, the problem is not lack of wealth at all. Nor is it a lack of any specific financial system channeling savings into bonds or bank deposits for people to hold in their portfolio. The system is still channeling savings into capital-preserving vehicles too much and into equity, scale and venture-based finance too little and the reason for that remains largely misunderstood.

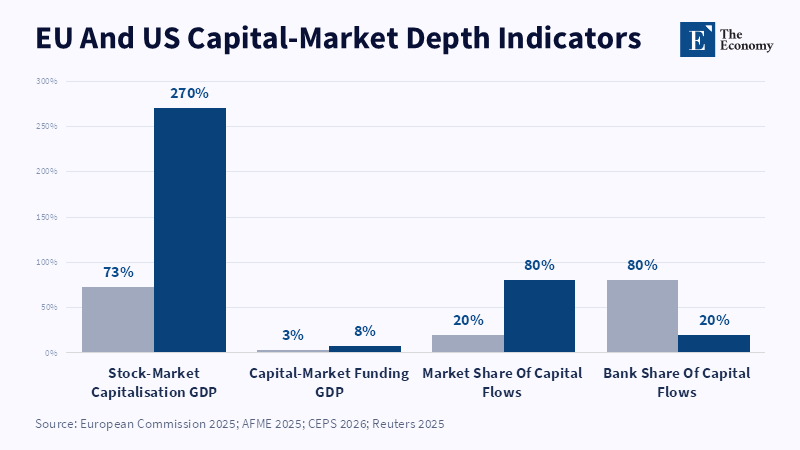

More recent official evidence confirms this. By 2025, the European Commission conceded that EU financial markets remain significantly fragmented, small and lack competitiveness[6] and in 2024, stock-market capitalization in the EU was 73% of the EU GDP, down from 270% in the United States.[7] As AFME's 2025 CMU indicators have also demonstrated, in the same year, EU corporates obtained only 13% of their total financing from market-based sources[8] and total private and public capital-market financing in the EU had remained stuck at around 3% of GDP, between 2020 and 2024, whereas the US had reached 8%.[9] These findings suggest that the EU's financial system still intermediates savings along paths that reinforce incumbent-heavy economic structures instead of amplifying the continent’s allocative dynamism. The issue is not just that Europe is a smaller version of the US in certain specificities of the markets. The issue is that Europe's financial system, despite its size, too often fails to convert a sizable pool of savings resources into productive risk capital.

That relative weakness is more consequential between 2023 and 2026 because Europe's strategic needs have changed. Europe is being asked to underwrite rearmament, decarbonization of its industries, semiconductor and AI capability, energy security and a faster scale-up of technology firms under conditions of geopolitical stress and weaker external demand. The Commission's Savings and Investment Union strategy in March 2025 and its market integration and supervision package in December 2025 were a clear acceptance that the current configuration is not providing incentives for savings going forward.[10] It is no longer a matter of whether Europe needs deeper capital markets in the abstract, but whether it can reconfigure the institutions, incentives and financial geography that reinforce savings dominance in safety, segmentation and external markets. On that issue, the right response is neither fatalism nor complacency. Europe's financial undershoot is not a given. But it is built into a set-up that financial-sector pressure alone cannot change.

The argument outlined so far appears to be quite simple. While European institutions do seem to be relatively inactive investors, that inactivity is primarily a function of the fundamental growth environment, the composition of product demand, pension schemes and regulators’ incentives. Financial markets in Europe are neither underdeveloped nor fully integrated; rather, they are segmented in a way that limits competition, size, liquidity and sophistication. And the notion that financial activity has stood in for, rather than to the side of, the European economy is false; the aftermath of the Brexit vote has not seen the emergence of a genuinely European substitute for London. Although London remains a systemically important financial center, it no longer provides the same hub-and-spoke continuum for the European project; this leaves Europe with a polycentric, specialized and less efficient system of equity price discovery than the US. The conclusion, therefore, cannot be attractive but unavoidable: European integration and growth are unlikely to come about without growth-friendly policy reforms, but growth will be hard to come by without a financial system more willing to fund new companies and the new economy. Finance is not everything. Yet a low-growth European economy will also be a low-finance economy.

2. European Financial Institutions Become Passive Because The System Rewards Caution

It would be easy to portray European institutional investors as culturally conservative or professionally unimaginative. It is not quite that simple a conclusion. The more robust analysis is that European institutions tend toward conservatism because the system around them encourages that. Financial institutions have balance sheets rooted in the promise of preservation of capital, duration-based asset-liabilities matching and the realization of incremental yield. EIOPA's reporting of occupational pension funds through 2025 indicated that by the end of 2024, European IORPs held around €2.69 trillion in investments[11] in their books and after look-through, it was revealed that the portfolio was concentrated on the 4 investment categories- investment funds, government bonds, equities and corporate bonds -also representing 92% of the assets.[12] On first glance, this does not look broadly inhibited- equities as part of a look-through investment were still somewhat significant. Yet this is precisely where the allocation problem becomes visible. The issue is not that European institutions take no risk at all. It is that the institutional architecture through which long-term savings are managed still rewards liquid, benchmark-conscious and easily defensible assets more than transformative risk-taking at scale. Portfolios may contain equities, but the system as a whole remains too weighted toward bonds, liability matching and domestically familiar instruments to provide the kind of patient capital needed for late-stage innovation and strategic industrial renewal.

The insurance side clarifies the mechanism even further. EIOPA's December 2025 Financial Stability Report stated that the largest share of insurers' and IORPs' investments has been placed into government and highly-rated corporate bonds.[13] It also highlighted an important prudential asymmetry: Government bond concentrations are not penalized under Solvency II in the same way as concentrations in corporate bonds or loans, where issuer-level capital requirements increase when holdings surpass certain thresholds.[14] This does not imply that regulation is structurally pulling these institutions into sovereign debt. It does imply that the supervisory regime systematically encourages capital to be liquid, high-quality and easy to justify. A manager that prefers government debt is not just choosing between risk and return – it is responding to the combined effect of liabilities, capital treatment and the rules under which the institution is managed. In this context, passivity is often more a sign of a rational market equilibrium than failures of foresight.

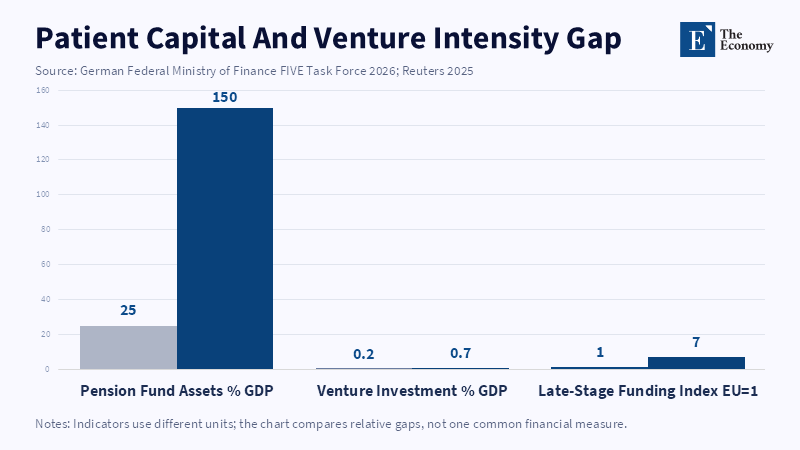

That is compounded by Europe's pension structure. A 2026 paper prepared for the German finance ministry's 'FIVE' task force argued that Europe's scaling-up deficit is explained by the absence of deep pools of patient capital resulting from pension design, institutional risk aversion, regulation and intra-market fragmentation.[15] Its most revealing comparison is instructive: pension fund assets in the EU are only about 25 percent of GDP, compared to roughly 150 percent in the United States.[16] That shortfall matters because funded occupational pensions produce long-duration balance sheets fundamentally well matched to equities, venture and other illiquid growth capital. Where retirement provision remains largely pay-as-you-go, the stock of long-duration private capital is correspondingly less resilient. In this sense, the European-US contrast is not simply between competing management styles. Instead, it poses a choice between, on one side, the promotion of a large pool of privately supplied, risk-bearing retirement capital and, on the other, reliance on public redistribution coupled with banking finance, followed by limited appetite for late-stage equity risk.

The scale-up implications are quantifiable. The same taskforce report, published in 2026 but relying on some IMF evidence, noted that venture investment in the EU was circa 0.2% of GDP in comparison to approximately 0.7% in the United States;[17] that over the course of the previous ten years, fewer than 35 megafunds in excess of 500 million had been raised in the EU;[18] and that funds in excess of $1 billion constituted less than twenty percent of European VC fundraising between 2020 and 2023, as opposed to around forty percent in the United States.[19] The gap is at its most acute precisely at the points where capital markets are, in the words of the report, most important: late-stage rounds, pre-IPO investing and the critical crossing-point from a technology's promise to its worldwide proliferation. The report also identified that, although European investors tend to dominate in seed capital rounds, their proportion drops markedly during scale-up rounds.[20] This stark drop is the cardinal point: Europe can often develop interesting firms. It finds it hard to sustain capital shares in them when they are likely to be of strategic importance.

The growth environment is therefore central. Risk is not allocated by financial institutions in a vacuum: they time it to the opportunity set offered by the rest of the economy. If less to offer in terms of relatively fast-growing firms, fewer relatively scalable champions in the technology space, shallower channels for exit and lower-price expected earnings acceleration, conservative portfolios are not simply an institutional pathology; it is an endogenous outcome to the shared state of low expected returns. This, too, is where the comparison with the United States, often overstated in rhetoric, still proves germane. Mid-2025 projections of OECD growth showed 1 percent euro-area GDP expansion in 2025, 1.2 percent in 2026, despite the recently revised trade policy outlook, while the United States was slated to grow 1.6 percent in 2025 and 1.5 percent in 2026.[21] The exact figures may change with the cycle, but the broader structural point is that, for most of the post-2023 period, the United States still offered a far more continuous environment for listed technology champions, late-stage private funding and highly visible exits. That deeper channel also attracts the European savings. According to EIOPA's IORP factsheet, European occupational pension funds had a total of €291 billion in equity exposure to US companies.[22] These European institutional investors appear willing to hold U.S equities when they had to be exposed to equity risk.

This point becomes important precisely because it rectifies a misconception. The problem with Europe is not that its institutions cannot bear risk: it is that they often choose to bear risk elsewhere (e.g., their significant holdings of US equity securities, as discussed in the previous section). The fact that European institutional investors have a large amount of money invested in foreign markets, such as US technology stocks and European-financed technology firms listed on foreign exchanges, is evidence of the allocation problem. It is not simply a problem of bond versus equity investment: in Europe, there is an additional dimension of the home versus the rest of the world. If Europe ex-ante invests all its savings in US-listed tech firms while underfinancing European technology, one cannot simply interpret this choice as conservative: the issue is not risk avoidance, but selective risk-taking outside Europe. Bruegel's intuition about the importance of an incremental point of investment seems to be stronger than the possible econometric evidence of the present paper: what matters is not just the portfolio mix, but also the jurisdiction of the risk capital. That Europe's households and institutions are already part of global growth is indisputable; that they are part of European growth in particular is not.

Household preferences extend this logic. The Commission 2025 Savings and Investments Union plan pointed out that as much as 70 percent of household savings in the EU – about 10 trillion – were still in bank deposits.[23] That observation is not simply an interesting historical fact. It is a sign of a political economy of intermediation. Retail savers who prefer the security of deposits make a liability structure that is convenient for banks, reinforces prudent retail distribution models and makes ever-deeper retail equity participation less necessary. Deposits are stabilization devices for households and banks; thus, this is not an irrational choice on an individual level. However, at the systemic level, deposit balances high enough to remain stable also have the effect of locking up the euro zone economy's capital in low-returning channels and of strengthening Europe's bank-centric financial architecture. This is why solely placing blame at the feet of institutional managers is simply too easy. The social conservatism precedes the managerial choice. Customers prefer products that protect their nominal principal; institutions design and price their products to those preferences; supervisors seek to both accommodate these preferences and optimally control them; and the end result is a savings-rich but growth-poor continent.

The best counter to this diagnosis should be taken seriously. Caution can be a virtue. Europe's aging population, its welfare state burden to protect retirement savings and its banking system as the continent's premium macro-financial stabilizer make the case for conservative inter-institutional allocation-protecting against excess risk and excess boom-bust swings-compelling. There is truth in the logic. But it is at the risk of the microprudence to macrooptimality link that it muddies: the 2024 OECD evidence shows that, among pension plans, the highest equity exposure was associated with some of the strongest investment performance.[24] And yet a system-wide level can be failed by what is prudential at the narrowest level, as long as it underdevotes long-term equity capital to innovative enterprises. Europe's problem is not that prudence is always inappropriate. It is that individually prudent choices aggregate into ultimately weaker capital-market development.

The conclusion naturally flows from the diagnosis. Europe does not need to enforce reckless portfolio shifts. It needs to change the environment that makes timidness the obvious choice. This involves opening up supplementary pension schemes where they are not yet sufficiently financed; providing simple, tax-efficient, long-term retail investment vehicles that can beat deposits; adjusting prudential standards where they produce excessively disproportionate treatment of sovereign versus productive private assets; and providing credible domestic capacity for scale-up for institutions so that they can justify more equity risk within Europe rather than abroad. It also involves recognizing that finance is unable to escape the economically driven nature of markets. Absent a step change in productivity, an increase in scale-intensive enterprises and the deepening of technological industrial clusters, institutional portfolios will continue to appear conservative for reasons more macroeconomic than cultural. The customer, the authority and the real economy are all part of one allocative system. This is why financial inertia in Europe needs to be thought of not as an ethical failing of institutions but as a structural consequence of the economic environment in which they operate.

3. European Financial Markets Are Fragmented Before They Are Underdeveloped

If the first problem is institutional design, the second is the structure of the market to which those institutions are directed. Underdeveloped is a useful, although oversimplified, term. But fragmented is a more accurate description. Europe is not deficient in financial talent or product expertise.However, it does lack an integrated market of sufficiently great breadth, depth and consistent rules to produce the significant network effects that market sophistication needs to thrive. CEPS reasoned in 2024 that Europe's banking markets, markets of financial instruments and enforcement of financial regulation across member states were still fragmented.[25] The EC's comments in 2025 were more explicit still: The EU financial markets are fragmented, small and not very competitive. These aobservations are substantively important. After a decade of trying to complete the Capital Markets Union, the European Commission is effectively acknowledging that the project has not achieved the critical mass.

The quantitative asymmetry with the US is sufficiently large to matter at a macroeconomic level. According to the Commission's 2025 market integration package, stock-market capitalization levels in 2024 stood at 73% of EU GDP versus 270% in the US.[26] AFME's 2025 indicators found that the level of market-based finance in the EU accounted for just 13% of all corporate funding[27] and that the level of new capital-market funding between 2020 and 2024 had remained stable at 3% of GDP versus an 8% in the US.[28] These statistics matter not because every economy should be run along the lines of the US financial system, but because they expose how shallow secondary markets can bear on primary-market choices: thin public markets acts as a drag on listing valuations, as it depresses market liquidity and analyst coverage, as it squeezes angel investors and venture capitalists; finally and paradoxically, it makes early-stage risk-taking less attractive. Today doesn't just matter to a growth firm's future fundraising plans. Tomorrow's exit environment does too. And the evidence from Europe is still underwhelming.

That is why the mere count of institutions or assets fails to come to grips with the measures of financial sophistication. A sophisticated market is where investors of varying risk preferences can find each other at scale, where specialized intermediaries invest in research given sufficient deal flow and trading activity, where secondary listings facilitate predictable prices set by often-informed sellers and buyers and where success stories alter expectations for entrepreneurs and institutional players. Europe has sophisticated local clusters and capable firms. It does not yet have a tight continental market that effectively translates those local strengths into a robust, scalable and self-reinforcing risk-capital ecosystem. The difference is fundamental. Financial sophistication is not a catalog of product offerings. It is an emergent phenomenon of scale, competition and expectation.

The underlying problem is the incomplete single market. Following the European Commission, the IMF has estimated that the rate of remaining intra-EU barriers amounted to a tariff of roughly 44% for goods and 110% for services.[29] Such measurements refer to the wider single market but have a direct bearing on the financial market, as financial markets are assumed to be, to some extent, integrated with product/service markets in the long run. Thus, developed financial markets with many large firms to make a presence and a lot of analysts working on a whole bunch of these firms,are hardly reachable if the distribution of insolvency regimes, tax rates, listing requirements, supervisors, clearing and settlement systems, consumer rules, or administrative costs continuously differ across countries. It follows that by reducing their effective size (say from 370 million to a handful of hundreds of millions), fragmentation of the real economy engenders heterogeneity on the financial plane. This reasoning would give reasons for the continent with admittedly partial service integration not to meet dollar-like capital market depth.

The implications are clearest in Europe's funding escalator. AFME announced in 2025 that European IPOs had declined a further 23% even as IPO activity was rising 20-60% in the US, China, Japan and Australia.[30] Moreover, cross-border equity issuance remained limited in the EU, representing just 6% of all capital raising by EU companies[31] and languishing even as it had nearly vanished two decades earlier in the 10% to 14% range. And while a larger role for private markets is visible, this has yet to mitigate the problem. Hardening private pools offers the public markets a reprieve, but a gloomier exit environment ultimately finds its way back into private valuation and later-stage funding. The world could keep unicorns private for longer, but can no longer afford to be free from the real stock markets and broad-based investor interest. Europe's challenge is not the lack of private capital, but the continued fractures in the public-market layer above.

The evidence on scale-ups confirms this inference. The 2026 FIVE report observes that Europe's lack of late-stage venture capital translates into overseas listing and the partial relocation of activity,[32] but emphasizes that Europe's scale-up problem is not simply that of scarcer capital, but rather the fundamental lack of a large, sufficiently integrated and innovation-based market through which fixed costs can be spread with speed. This is the true meaning of fragmentation. It's not just a bureaucratic dimension. It alters the payoff matrix for growth-oriented firms. While crossing the US market still means crossing a single federal commercial market, crossing the EU regional divides often implies crossing multiple regulatory, tax, legal and supervisory thresholds and under certain conditions, the United States can still count on the comparative advantage of scale-up. Europe's capital-market weakness is at least partly a result of the broader political economy, in which the single market remains more in principle than in the commercial experience of entrepreneurs.

Home bias is both a symptom and a cause of this underdevelopment. The EIOPA 2025 stability brief suggests that insurers hold many times more illiquid and unlisted euro area corporate bonds domestically than liquid corporate bonds,[33] that assets such as mortgage, loans and unlisted corporate bonds are mainly home-country oriented without sharp foreign diversification.[34] This is relevant as segmented markets tempt institutions to operate as domestic carry investors rather than pan-European allocators of growth capital. As long as illiquid balance sheet assets are nationally concentrated, competition is relatively subdued, benchmarking is less international and corporate funding circuits are delimited. The consequence is a European savings box that looks internally rich rather than externally integrated. This is another argument why Europe may not only have a large financial industry but an ineffective one at the same time. Size but not integration can imply surface action but subsurface irrelevance.

Here too, the strongest counter-argument requires the most weight. One could, of course, argue that the contention that Europe is fragmented is largely an overstatement, because, among other reasons, Europe is home to globally competitive asset managers, large insurers, successful exchanges and globally active sovereign and corporate bond markets. This appeal has some truth to it. Europe is not a financial desert. EFAMA announced record assets of €33 trillion in 2024[35] and, according to the same source, at the end of that year, the European asset managers held some 6.8 trillion (or 28% of the total EU debt securities) and around 2.9 trillion (or 24% of the listed EU shares,[36] on that year's published figures). Europe does have financial power. What it does not have is that power widely spread and sufficiently reconfigured into a united competitive arena of capital markets. The existence of major asset managers does not figure against fragmentation; in fact, it lives side by side with it to some extent. Europe can already boast a group of truly global dominant intermediaries and yet still lacks that integrated market system that would allow such agents to catalyze the domestic risk-capital formation.

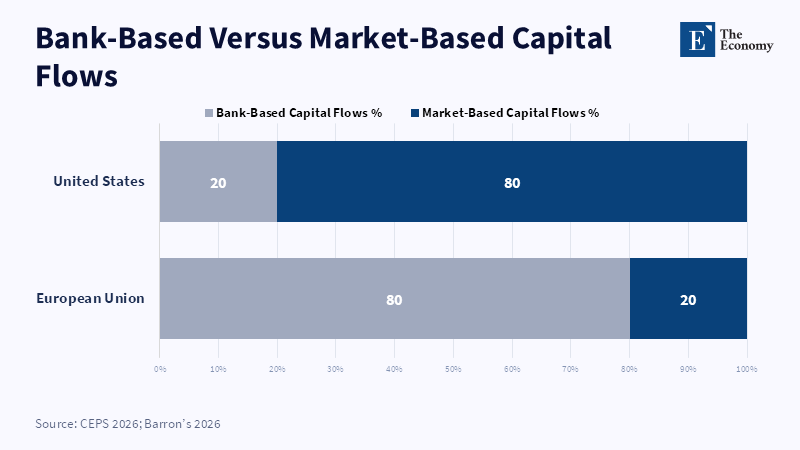

A second counterargument suggests that Europe is simply adopting a different, yet equally successful approach: a bank-based system which offers more sustainable funding of the real economy than market-based finance and thus is more valid. This again is partly correct. Bank finance is crucial, especially for SMEs, households and cyclical stabilization. But the real question here is not whether Europe needs to move away from banks. It is whether a system in which bank intermediation dominates can absorb the high uncertainties, intangibility and technology-optimized (yardstick on scale, data and optionality, rather than collateral)of expensive frontier sectors. On this frontier, empirically, bank-based finance is notably impoverished. It is not a coincidence that the IMF, the commission, the ECB, the EIB and indeed all national policymakers and regulators have returned to the same conclusion: Europe must get stronger, with regard to equity and venture capital sectors, precisely because the development role that bank-lending performs for most frontier sectors simply does not carry over. The bank-based approach is not incorrect. It is incomplete.

The policy recommendation is therefore neither more markets in abstract nor indeed more capital markets. Europe does, after all, need fewer national barriers in issuance, settlement, insolvency, taxation and market regulation, not more; indeed, it needs a stronger center where scale effects are unequivocal. It needs relatively simple and standardized infrastructure vehicles for household investment in equities and a coherent framework for capital markets to link private and public exit strategies. Practice demands nothing less than sidelining the declaratory aspect of the Capital Markets Union and treating integration as industrial policy. Furthermore, it requires the discipline of not imposing unnecessary rules but rather responding to well-informed payoffs that give markets contestability, scale and liquidity. Europe has had the accumulated savings to support such a system for ages. What it has not had is the institutional capacity and political will to integrate the single market for finance. Until this political constraint is overcome, underdeveloped and fragmented will be interchangeable.

4. Post-Brexit Europe Lacks A Single Financial Center

The suggestion that after Brexit there is no longer a financial center in Europe is too sweeping if taken literally. The City is still undeniably Europe’s most important international financial center. Evidence from the BIS 2022 Triennial Survey showed that London was still dominant in foreign-exchange transactions in 2022 and has retained a significant lead in international banking,[37] even as it continued to lose share in euro interest rate swaps against euro area centers. The 2025 edition of the Global Financial Center Index continued to rank London as the second most important financial center in the world, far ahead of Frankfurt, Paris, Luxembourg and Dublin.[38] Any attempt to treat Brexit as an indication of the end of the City as a global financial center is, therefore, weak analytically. London is still one of the very few truly global financial centers in the world. That must be the sober truth, because policy-making on a comforting lie can only go wrong.

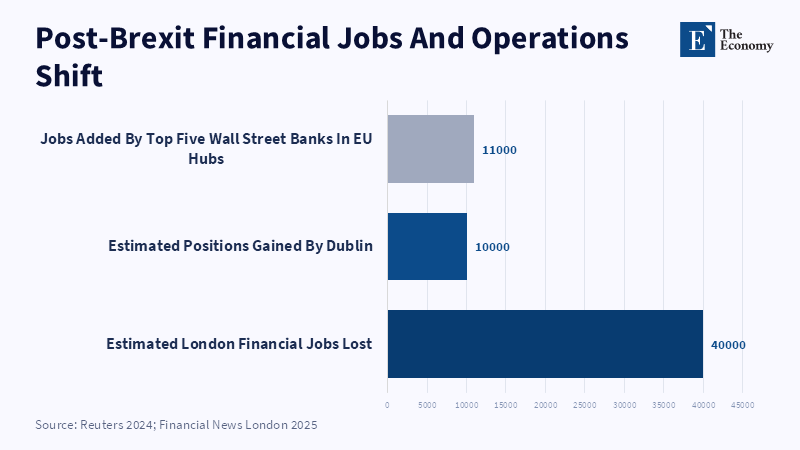

Nonetheless, the policy-relevant core revision of the claim is mostly right: Europe does not now have a single financial center that combines the density of London's capital, its reach into global markets and locales and its status as a core of specialist ecosystems, with the seamless integration into the legal and regulatory architecture of the EU. That is the real loss. Brexit didn't take London out of the picture; it finally drew a line under the extension of Europe's most advanced financial cluster into the single market it used to operate from inside. But the result has not been continuity, nor a clear one-to-one replacement; it has been the unbundling of Europe's financial functions. New Financial's 2021 analysis mapped over 440 firms that had set some part of their business, employment, capital, or legal infrastructure an average of just over 250 kilometers east of London,[39] which at the time was further than any other European center and more than US $900 billion of bank assets that had been shifted or announced for shifting.[40] The broad makeup of the beneficiaries was functionally dispersed. Dublin led in the number of firms; Paris and Frankfurt drew contrasting types of activities; Luxembourg maintained its long-term relevance for funds; Amsterdam gained a major share of cross-border trading and market infrastructure. But the meta-conclusion in the report was telling: no one jurisdiction at a macro level emerged as dominant; activity was dispersed both by environment and by type.

Later work, however, argued that this reallocation was not a discrete event but a continuous process of reorganization of financial services. In 2025, the Economics Observatory found that UK firms had exported less and invested more abroad since Brexit, with 46% of greenfield investments and 69% of M&As between UK-based financial firms between 2016 and 2023 going to the European Union.[41] That trend signals something profound: it suggests that providing service within the Union to European customers increasingly requires establishing firm-specific presence inside Europe itself, rather than the traditional ability to provide cross-border wholesale services from London. In short, London remained an undisputed global financial capital, but its ability to intermediate European markets from outside was lost. The old one, where the continent effectively offshored wholesale capital markets intermediation to London, while relying on offshored political clout, has been disrupted and no serious alternative in the same density has grown up yet.

And this is why the resilience of London and the weakness of Europe can coexist. BIS has confirmed that London has still been dominant in FX and strong in banking activity; however, they have also found that its links to the euro area have further weakened,[42] partly a consequence of the move of euro repo clearing from London to Paris. Academic and policy commentaries in the aftermath of Brexit have repeatedly characterized the new configuration as fragmented and specialized rather than centralized and hierarchical-one city reigns in trading and another in banking supervision, one specializing in funds and domiciliation and a third in law, tax and other vehicles. Such a network can sustain compliance with EU-level rules on market access; it cannot inherently create the rich informational ecology of a single center of gravity. Equity market price discovery- particularly for growth firms-relies not just on formal access, but on density, analysts, sectors, specialists, institutions, lawyers, bankers and repetitions. Europe's post-Brexit map is capable of functioning, but far too spread out to challenge New York at the head of equity finance.

The symbolic significance of Arm's 2023 New York listing is here. Reuters has reported that SoftBank elected a US-only listing for Arm, explaining that New York was the 'best path forward,'[43] with the London Stock Exchange itself arguing that the choice merely confirmed the need for reform in UK markets. The follow-up broad trend for listings since then has further substantiated the indication: Reuters 2025 reflections on how more companies are moving away from London to bolster investor demand and correct UK valuations identified both aspects as recurrent rationale for switching primary listings or selecting the US.[44] Arm's choice was not just an insult to London. It was a market expression of where a profound technology enterprise anticipated to reveal a broader investor field and more compelling valuation support - and that expression must be disturbing not just for Britain, but for Europe more generally, because London once was the continent's closest proxy to a New York-type capital-markets hub. If even London itself failed to retain such a listing within the confines of its own ecosystem, the challenge for Paris, Frankfurt, or Amsterdam should be evident.

Some nuance, however, for the Arm example. Too often ASML appears to be taken to excess as well. It is not a story of a European champion leaving Europe for New York. Its core listing remains Euronext and it has one in New York as well.[45] That makes a difference. But it does not change the bottom line. Quite to the contrary: it illuminates it. Having investable instruments in two markets demonstrates that even Europe's most strategically vital listed tech firm still finds direct access to US capital markets essential. The conclusion is not that every key European business needs to run from the continent. It is, rather, that the most globally critical European companies regularly appear to see U.S. markets as necessary for liquidity, valuation, or investor support; and that a continent seeking to secure strategic independence in tech and manufacturing should be uneasy with such disparities.

Why then has no clear successor appeared? The first reason is one of political rivalry. Paris, Frankfurt, Amsterdam, Dublin, Luxembourg and others have all, to some extent, gained something by their new placement and have little to gain from meekly yielding global dominance. The second is one of functional specialization-this means there is a multi-center equilibrium that is desired. The third is that London's advantages in agglomeration have taken many years for their sources to develop; such advantages cannot be quickly generated through administrative instruction. An international financial center is more than just regulation plus office space; it is the complex ecosystem of tacit knowledge, dense labor markets, legal expertise, financial media attention and repeated transactions in which they are embedded. That is the nature of the problem that New Financial poses-even while identifying some significant post-Brexit relocations, it is able to consistently assert that London is likely to continue to be the pre-eminent financial center in Europe for the near future.[46] The problem for the EU is not that London disappeared but that it continued to dominate, albeit externally, without the benefits of having the capital inside the EU's regulatory framework.

The policy implication has no more of a European Wall Street question than many of the standard calls for a European Wall Street do. It can't be that one city is better than all the rest, it is hardly likely, desirable and conceivable to dictate as policy. Yet a truce for a purely laissez-faire polycentric equilibrium would be constrained. If Europe is to countenance a permanent polycentricity with zones of specific competence across the EU, then since the network where it really counts needs to work up to and including a single market-more stringent central oversight when needed, harmonized conventional investment and post-trade listing and infrastructure rules on a real-time basis and an explicit move to consolidate equity-market liquidity rather than lower aggregate trade via various national divides-would be needed as a practical matter. At the same time, there remains macro-economically feasible ground for a pragmatic EU-UK financial reset.[47] That is the central dilemma in the macroeconomics of 2025. Either Europe will continue to absorb London whenever possible through structured EU-UK financial cooperation, or it will persist in living in a suboptimal equilibrium where London is the world, EU centers are regional and New York still is the unique location for world-class equity finance.

5. Conclusion - From Savings Abundance To Productive Risk Capital

Europe's financial weakness is often treated as if it were narrowly financial. It is not. It is the market-based form of a deeper economic structure. The continent has a surfeit of savings, huge asset management businesses, large internationally active banks and insurers and several successful financial centres. All of these, however, are still directing too much household wealth into deposits, too much institutional capital into low-innovation fixed income securities, too much risk appetite into US assets, too little long-duration financial intermediation into Europe's growth sectors. That's why the critical breakpoint is not just size versus allocation, but allocation within a fragmented single market that lacks an internalised financial centre.

Therefore, the policy response must go beyond the capital markets rhetoric. Europe requires deeper funded pools of pension capital, more efficient mobilization of retail investment, prudential rules that do not inappropriately channel the perceived safety of sovereign investments in favor of productive diversification and far deeper integration of supervision, insolvency, listing and market infrastructure. It also needs, critically, growth engines in advanced manufacturing, defense, energy and frontier technology that are capable of vastly increasing the expected return to risk capital. Finance can amplify growth, but it cannot create it through administrative ambition alone. That is the last lesson. Without stronger fundamentals, financial liberalization will fall short. But without financial liberalization, stronger fundamentals will simply shift more and more to those more capable markets, equipped to price and fund them. Europe's strategic autonomy will stay unachieved, as long as its savings do not just become plentiful, but are optimally used and so long as they are so widely dispersed.

References

[1, 2] Bruegel (2026) Size versus Allocation: Capital Market Development, Evidence from Pension Funds and Insurers. Bruegel Working Paper.

[3, 4, 10, 23] European Commission (2025) Savings and Investments Union: A Strategy to Foster Citizens’ Wealth and Economic Competitiveness in the EU. European Commission.

[5, 35, 36] EFAMA (2025) Asset Management in Europe: Facts and Figures. European Fund and Asset Management Association.

[6, 7, 26] European Commission (2025) Market Integration and Supervision Package: Capital-Market Indicators. European Commission.

[8, 9, 27, 28, 30, 31] AFME (2025) Capital Markets Union Key Performance Indicators: Eighth Edition. Association for Financial Markets in Europe.

[11, 12, 22] EIOPA (2025) IORPs Statistics Factsheet Q4 2024. European Insurance and Occupational Pensions Authority.

[13, 14, 33, 34] EIOPA (2025) Financial Stability Report December 2025. European Insurance and Occupational Pensions Authority.

[15, 16, 18, 19, 20, 32] German Federal Ministry of Finance / FIVE Task Force (2026) Financing Innovative Ventures in Europe. Federal Ministry of Finance.

[17] IMF (2024) Stepping Up Venture Capital to Finance Innovation in Europe. International Monetary Fund.

[21] OECD (2025) OECD Economic Outlook, Volume 2025 Issue 1. OECD Publishing.

[24] OECD (2025) Pension Markets in Focus 2025. OECD Publishing.

[25] CEPS (2024) Why We Need to Rewire Europe’s Financial Sector to End Fragmentation and Bolster Integration. Centre for European Policy Studies.

[29] IMF (2024) Europe’s Choice: Policies for Growth and Resilience. International Monetary Fund.

[37, 42] Bank for International Settlements (2022) Triennial Central Bank Survey of Foreign Exchange and OTC Derivatives Markets. BIS.

[38] Z/Yen and China Development Institute (2025) The Global Financial Centres Index 37. Long Finance.

[39, 40, 46] New Financial (2021) Brexit and the City: The Impact So Far. New Financial.

[41] Economics Observatory (2025) How Has Brexit Affected UK Financial Services? Economics Observatory.

[43] Reuters (2023) SoftBank’s Arm to Pursue U.S.-Only Listing. Reuters.

[44] Reuters (2025) Companies Leaving London Seek Deeper Investor Demand and Stronger Valuations. Reuters.

[45] ASML (2026) Shares and Listings. ASML Investor Relations.

[47] Bruegel (2025) EU-UK Financial Services and the Post-Brexit Economic Reset. Bruegel.