Europe’s China Risk Is Not Where the Trade Deficit Says It Is

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

EU trade de-risking should not be driven by import shares alone The real risk lies in concentrated, hard-to-replace inputs Europe needs selective resilience, not broad decoupling

EU trade de-risking could fail in two completely different ways. Europe might do too little at the few points where a disruption in supplies would shut factories down or it might go much further than is sensible at thousands of straightforwardly replaceable imports. The latter would not be cheap. OECD modeling shows that a general move towards re-shoring production would slash global trade by over 18% and world real GDP by around 5%, even when not every economy is made more resilient. This evidence should redouble the seriousness of the debate. A large trade deficit is not a sign of risk and a high import share should not be accepted as a sign of fragility. The real peril lies in a tiny selection of products with concentrated supply, slow substitution and a disproportionately large part to play in final output. EU trade de-risking needs a clearly defined mandate. Europe has to identify which dependencies can be alleviated, which can be shifted and which could shut down vital systems before an available alternative can be found. What is needed is not less trade on a whim, but less exposure to shocks which firms cannot counteract in time.

EU Trade De-risking Starts Where Import Shares End

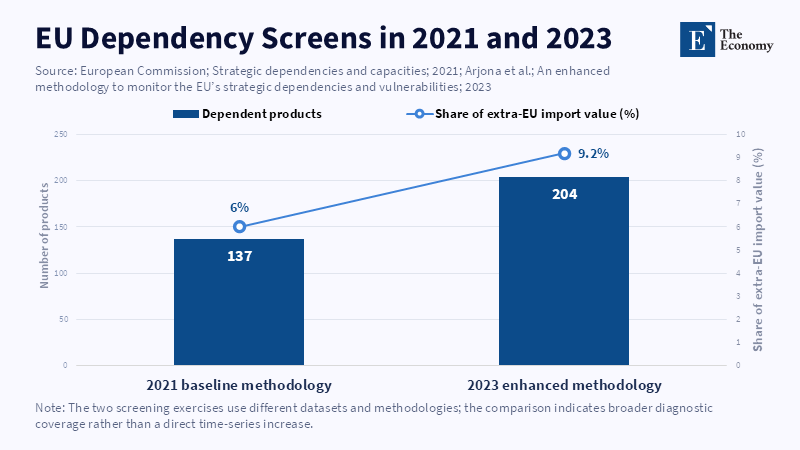

The first step is to separate the commercial from the strategic. Europe may buy the equivalent of a third of China’s exports as a whole. Yet, the large volume of that reliance indicates little about the current economic damage a break might cause. The Commission's first trade dependency barometer in 2021 identified 137 products in sensitive sectors with very high reliance. They represented around 6 percent of extra-EU import value. A wider and more detailed one in 2023 identified 204 products and lifted that share to 9.2 percent. That increase was not evidence of collapse across the economy, but of how screening improvements identified narrower lines of dependence. The key point is that the important distinction is not how many goods the EU imports from China but how quickly industry’s needed capabilities can be maintained in their absence.

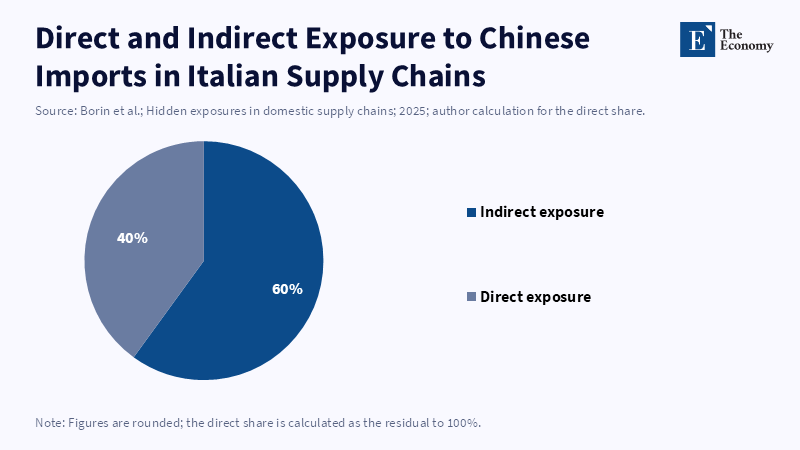

Trade data also hides where a shock would propagate through the economy after goods cross the border. Firm-level research on Italy shows Chinese imports account for about 3.6 percent of costs, but close to 60 percent of that exposure went through domestic buyer and supplier links. In about 90 percent of local labor markets, indirect exposure was greater than direct exposure. This explains why a customs ledger can be quiet, while a production network is brittle. The same insight applies to euro-area modeling. A halt in critical inputs can generate a twenty times larger slump in final demand than the initial share of inputs withdrawn. The modeled euro-area slump increased from 0.04 percent in 1995 to 0.41 percent in 2023. These were not predictions of an inevitable crisis. They merely illustrate how bottlenecks are able to amplify a small trade shock. EU trade de-risking must therefore reflect internal transmission, not just border flows.

EU Trade De-risking Needs a Three-Part Test

The overall sound test has three elements: import vulnerability which detects the proportion of imports, the share of the biggest supplier, active suppliers, trade partner position and trade flow reliability; substitution difficulty which seeks to establish presence of else-where producers and whether they are able produce to a given standard as well as the time a firm takes to qualify external sources; and industrial criticality, whether a good is linked to many other sectors and to public goods infrastructure or a key enabling technology. Only when all three elements overlap should the strongest policy action follow. A concentrated product where easy substitutability is available should trigger a shift to search and contractual improvements. An easy-to-supply product that is not yet concentrated warrants an early warning. A hard-to-supply product that is concentrated and integrated very deeply into production is the ultimate hard case. However tough EU trade de-risking may prove to be, this three-part test provides a clear guide. Policy must escalate with the likely impacts and the time to rebuild.

The test must also assume the future. The current trade records show the countries from which the goods came over the last year. But they do not show whether the world markets are concentrating into fewer hands, whether models or patents will block entry or whether a new supplier can clear safety inspections. And they do not show who owns the strategic process know-how, which, as the evidence often does, is what really matters. This is where the concept of managed interdependence is critical. Work on sovereign artificial intelligence has shown that control is never binary. A country may depend on foreign chips but still retain national jurisdiction over its data, its emerging models or its usage in the public sector. Trade resilience follows the same logic. Clearly, Europe would not need to own every mine, every plant and every patent. But it would need enough options so that no single supplier would have a veto over its operations. The next policy tool would be an indicator of active frontier products. Customs records should be combined with business surveys, input-output tables, inventories, licensing times, dual ownership records and evidence of increased primary global concentration. EU trade de-risking should measure its evolution.

The missing link is governance. Europe has many risk measures, but they tend to be cast in separate boxes. Trade officials monitor imports. Industry teams fund projects. Competition authorities screen state aid. European ministries have contingency powers, while firms hold valuable data. An EU standing supply risk monitoring center should link those groups. It should issue the methodology and general risk ranges, safeguarding firm-level data. Member states should reveal stockpiles and contingency regimes. Large buyers in chosen sectors should reveal single-source inputs and credible switch-over timings. Single-source procurement should be awarded to a second qualifying bidder if the extra cost is modest. The center should also examine whether the risk declines after support begins. Without such feedback, temporary aid can become protection in perpetuity. With it, EU trade de-risking can function as a cycle: detect, trial, impose and back off once a market has become sufficiently deep.

EU Trade De-risking Must Match the Type of Risk

A risk map is a useful tool only if it influences policy response. For vulnerable goods with substitutes that are simply available, the course of action may be to do little apart from monitor and promote open trade. For vulnerable commodities with a simple substitute, the prescription is diversification, which may not mean production elsewhere but rather a trade deal, a second qualified supplier, export credit or a competitive tender that rewards redundancy and fortitude. For the less vulnerable goods with a questionable or hard-to-access substitute, the priority should be preparing in advance, extending contracts, maintaining small precautionary stocks, fostering shared standards and giving financial backing so a painless choice always remains. The strong prescription for highly vulnerable commodities with a questionable or difficult-to-rely-on substitute is the maximum package including strategic stocks, recycling, long-term offtake, allied production, rapid procedures and some backup for new capacity. Such a classification prevents the establishment of EU trade de-risking as a catchphrase. It also places limits on the use of state aid; public spending should not focus on visible industries or saving every enterprise and those commodities that are slow to adjust to market forces and have an externality-driven high cost of downside.

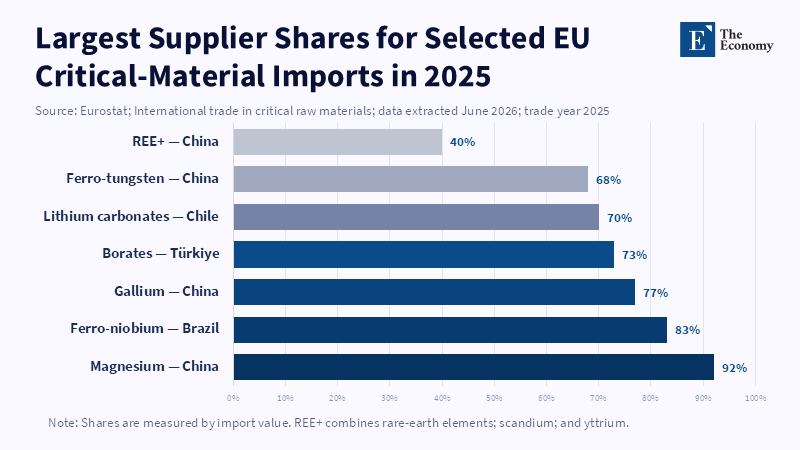

Solar panels and magnesium illustrate why the same share of imports can have very different policy implications. In 2024, China supplied 98 percent of the EU’s extra-EU solar-panel imports; that degree of concentration is extraordinary. But finished modules can be stockpiled, projects postponed and it is possible to purchase modules according to certain standards. The threat may be more distant: cells, wafers, processing machinery, the erosion of European manufacturing capability. Magnesium poses a different challenge: in 2025, China made up 92 percent of EU magnesium imports. Magnesium goes into cars, airplanes, electronics and metal production. A shortfall could affect several sectors for some time while new production ramps up, given the high energy costs. Both cases require investment: one, tariffs on finished modules, seems unlikely to address upstream reliance; the other, magnesium, may also require strategic reserves, recycling, electricity price support and lengthy contracts with new providers. Although the examples are different, the de-risking solution cannot be the same.

The EU has already embodied this logic within the Critical Raw Materials Act with a 2030 set of objectives, requiring at least 10 percent of the consumption of certain raw materials in the EU to be extracted there, 40 percent processed inside and 25 percent recycled. Among other objectives, Brussels proposes to limit dependence on a particular non-EU source to no more than 65 percent for each strategic material. Those targets are fine because they do not impose total autonomy. They provide a minimum capacity and a maximum dependence on a single third-country source. But targets alone will not produce resilience. A mine without processing is a fragile supply chain. A processor with unstable power or purchasers may close. A stockpile with no mechanism for government release is vulnerable in a crisis. EU trade de-risking will require contracts and institutions alongside mills and smelters. Brussels should mandate strategic projects to secure offtake, use collective purchasing to benefit from scale and implement periodic stress tests. Support should decrease when a market becomes competitive. Resilience should be understood as a promise to provide a service under certain conditions rather than as an unending subsidy.

EU Trade De-risking Needs Discipline, Not Distance

The most compelling challenge is also a warning: diversification is expensive. More suppliers mean fewer economies of scale. Better inventories mean more opportunity costs. More local manufacturing needs more support. An allied supply may reinforce the dependency, not undo it. All those costs are real. They also make a case for accuracy, not for delay. The goal is not to replace China with one preferred partner. It is to reduce the likelihood that a single country, firm, route or process can cut off the supply. Reliance on an ally is not risk-free, but it may be more manageable in a system where contracts are respected, norms are common and disagreements are settled through robust institutions. The prudent test is recoverability. How many able sources? How rapidly could alternate supplies be introduced? What stocks are available? Which domestic output would fail first and how fast? EU trade de-risking should be answering those questions before tariffs, essential support measures or screening criteria are determined. Trade defense may shield EY producers against unjust trade practices. There is no particular insurance for a de-risked supply chain.

The initial forecast is the ultimate test. A policy that reduces commerce by more than 18 percent and output by about 5 percent in the name of safety is imprudent if it leaves most bottlenecks intact. Europe needs a smaller and tougher agenda. Publish a regular list of high-risk products. All sectors should run controls against limits on irreplaceable inputs. Common rules should be set for stockpiles and deliveries. Tariffs and subsidies should be used only where substitution is slow, spillovers are large and a functioning market can be created. EU trade de-risking must be product-focused, not country-focused. The trade gap will remain a potent political theme. The real threat will often be quiet: a chemical, magnet, alloy, part, license or process that costs very little until it cannot be obtained. Europe's challenge is not to end interdependence. It is to make such interdependence manageable before the next crisis exposes its flaws. The cost of doing so should be assessed against the difference between the cost of a factory line, power plant or public service that cannot be shut down suddenly.

This article is based on an original research article published by The Economy Research. For the original version, please refer to [EU vs. China] Beyond Import Shares: A Risk-Based Framework for EU Trade Dependence on China.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An Enhanced Methodology to Monitor the EU’s Strategic Dependencies and Vulnerabilities. Single Market Economics Papers, No. 14. Luxembourg: Publications Office of the European Union.

Attinasi, M.G., Boeckelmann, L., Gerinovics, R. and Meunier, B. (2025) ‘Unveiling the hidden costs of critical dependencies’, ECB Economic Bulletin, 5/2025. Frankfurt am Main: European Central Bank.

Borin, A., Conteduca, F.P., Leone, F., Mancini, M. and Zoi, P. (2025) How Global Are Local Supply Chains? CESifo Working Paper No. 12271. Munich: CESifo.

European Commission (2021) Strategic Dependencies and Capacities. Commission Staff Working Document SWD(2021) 352 final. Brussels: European Commission.

European Commission and High Representative of the Union for Foreign Affairs and Security Policy (2023) European Economic Security Strategy. Joint Communication JOIN(2023) 20 final. Brussels: European Commission.

European Parliament and Council of the European Union (2024) ‘Regulation (EU) 2024/1252 establishing a framework for ensuring a secure and sustainable supply of critical raw materials’, Official Journal of the European Union, L series, 3 May.

Eurostat (2025) International Trade in Products Related to Green Energy. Statistics Explained. Luxembourg: Eurostat.

Eurostat (2026) International Trade in Critical Raw Materials. Statistics Explained. Luxembourg: Eurostat.

Joshi, S. (2026) ‘Early lessons in the pursuit of sovereign AI’, Carnegie Endowment for International Peace, 17 June.

Kowalski, P. and Andrenelli, A. (2025) ‘Economic security and vulnerabilities in international supply chains’, in OECD, Economic Security in a Changing World. Paris: OECD Publishing.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.