China Opens Lithium Futures and Options to Foreign Investors, Eyes Greater Control Over Global Pricing

Authored On

Modified

Guangzhou Futures Exchange opens lithium futures and options to overseas miners and battery makers Beijing accelerates efforts to attract foreign capital by linking physical supply chains with derivatives markets U.S. expands domestic supply chain investment but faces mounting challenges reshaping a market dominated by China's value chain

China, the world's largest lithium market, is opening its lithium carbonate futures and options market to overseas investors. The move will allow foreign market participants to hedge price risk directly through Chinese exchanges, further strengthening Beijing's influence over global lithium price formation. While the United States is also expanding strategic lithium stockpiles and building domestic supply chains under the leadership of the Department of Defense, China's overwhelming dominance across lithium refining, processing and battery manufacturing is expected to remain a significant obstacle to Washington's efforts to defend its position in the market.

Dollar Margins, Yuan Settlement: Beijing's Calculated Blueprint for Yuan Internationalization

According to Asia-Pacific Mineral Financial Value Chain Analysis on July 8 (local time), the Guangzhou Futures Exchange (GFEX), one of China's major commodity exchanges, fully opened onshore trading of lithium carbonate futures and options to overseas mining companies, battery manufacturers and global trading firms outside China as of July 3. The opening covers the LC2607 (July 2026) lithium carbonate futures contract and all subsequent lithium carbonate futures contracts listed thereafter, as well as options based on those futures contracts.

Global commodity derivatives markets have long relied on the Chicago Mercantile Exchange (CME), the London Metal Exchange (LME) and the Singapore Exchange (SGX) for international price discovery. In the lithium market in particular, CME and LME have successively launched lithium futures products that have become the primary venues where miners, refiners, battery manufacturers, automakers and global trading firms manage price volatility. CME's lithium carbonate futures use Fastmarkets' China-Japan-Korea (CJK) spot price assessment as their settlement benchmark, which has become a key reference point for global lithium contracts and supply negotiations.

That is precisely why China has opened the Guangzhou Futures Exchange to foreign investors. As the world's largest lithium refiner and the biggest purchaser of lithium raw materials, China commands an overwhelming share of physical market transactions. Beijing is now pursuing a strategy of extending its influence in physical supply chains into derivatives markets, with the goal of shifting the global benchmark market for lithium pricing to Chinese exchanges. Allowing overseas miners, battery manufacturers and global commodity traders to participate directly in GFEX is widely viewed as part of a broader strategy to gain greater influence over global commodity pricing while simultaneously elevating the yuan's status as an international currency.

According to a GFEX notice, foreign investors may post margin in U.S. dollars, but all trading and final settlement must be conducted exclusively in Chinese yuan. Previously, only qualified foreign institutional investors (QFIIs) with limited eligibility had access to the trading pipeline. By fully opening the market, Beijing is positioning itself to channel offshore industrial capital into its domestic exchange ecosystem.

China Strengthens Pricing Power Through Its Physical Supply Chain

Although China possesses only about 16.5% of the world's lithium reserves, it is currently the world's largest importer of lithium ore and accounts for more than 70% of global lithium cathode material production. These advantages have already given China substantial influence across the battery processing and manufacturing value chain. That pricing power is increasingly reflected in trading activity. Since listing lithium carbonate futures in July 2023, GFEX has rapidly attracted liquidity. Trading volumes quickly surpassed those of comparable lithium contracts on the LME and SGX, while changes in China's physical supply-demand balance became almost immediately reflected in futures prices. With lithium refining and battery manufacturing concentrated in China, market participants have increasingly come to regard China's physical market fundamentals as the most sensitive signal for global lithium pricing.

The recent plunge in Chinese lithium carbonate futures following reports that Contemporary Amperex Technology Co. Ltd. (CATL) may restart its Jianxiawo lithium mine in Jiangxi Province illustrates the same dynamic. The mine emerged as a key market variable after operations were suspended following the expiration of its mining permit in August 2025. At the time, concerns over tighter supply drove both lithium prices and mining stocks sharply higher. When expectations of a restart later surfaced, Chinese futures prices immediately came under downward pressure. The market has effectively reached a point where regulatory decisions affecting a single Chinese lithium mine can move global lithium prices.

As a result, prices established on Chinese exchanges have already become one of the fastest indicators reflecting changes across the physical supply chain. While long-term production from Australia and South America, electric vehicle demand and battery inventory adjustments remain the fundamental drivers of global lithium prices, China's futures market has become the fastest venue for incorporating those developments into market pricing. As participation by overseas miners, battery producers and trading firms expands, the structure of global lithium price negotiations could also shift. Until now, spot assessments by international price reporting agencies and derivatives prices on overseas exchanges such as CME and LME have served as the primary benchmarks. However, as trading volumes and physical delivery activity expand on Chinese exchanges, yuan-denominated lithium prices could assume a far greater role in global transactions.

U.S. Lithium Strategy Faces China's Supply Chain Dominance

The United States, meanwhile, continues to increase investment in building domestic lithium supply chains. On July 7, the Defense Logistics Agency (DLA), an agency under the U.S. Department of Defense, issued a solicitation seeking proposals to supply approximately 36 million pounds of battery-grade lithium carbonate over the next five years. The agency requested bidders to submit fixed-price offers covering the entire five-year period while indicating that the government is prepared to spend between USD 1 million and USD 300 million under the contract. As lithium has become a critical battery material not only for electric vehicles and energy storage systems (ESS), but also for drones, communications equipment and precision weapons systems, Washington has elevated the metal to the status of a strategic stockpile resource.

Lithium carbonate prices have climbed by more than one-third this year amid stronger demand expectations and supply uncertainties in major producing regions including China and Zimbabwe. Against that backdrop, the Donald Trump administration has made securing critical minerals and reducing dependence on China a policy priority. The latest procurement initiative also aligns with the Pentagon's broader push to expand strategic reserves of critical minerals. The Department of Defense has already supported private-sector investment, long-term purchase agreements and strategic stockpiling for lithium, nickel, graphite and rare earth elements essential to battery and defense supply chains. More recently, the U.S. Army has explored providing military base land for critical mineral processing facilities as part of broader efforts to bring mining, refining and processing capacity back to the United States.

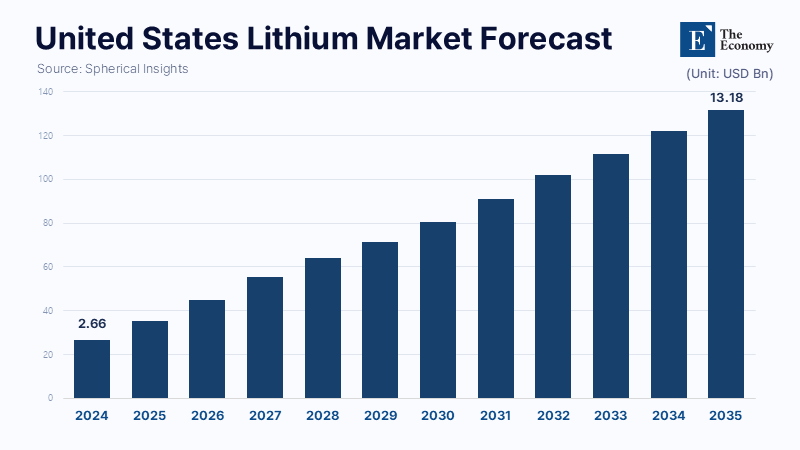

Growth prospects for the lithium market further support Washington's expanding supply chain investments. According to market research firm Spherical Insights, the U.S. lithium market is projected to grow from USD 2.66 billion in 2024 to USD 13.18 billion by 2035, representing a compound annual growth rate (CAGR) of 15.66%. Expanding electric vehicle adoption, rising investment in energy storage systems and additional battery manufacturing capacity are all expected to drive robust demand for battery-grade lithium. The U.S. government's parallel strategy of strategic stockpiling and supply chain restructuring is intended to prepare for that long-term increase in demand.

Yet the center of gravity in the global lithium supply chain remains firmly anchored in China. The International Energy Agency (IEA) estimates that China is the world's largest refiner in 19 of 20 major strategic minerals and holds an average market share of roughly 70% across critical energy mineral refining. China also dominates the battery value chain through its leadership in refining, cathode and anode materials, cell manufacturing and electric vehicle demand. Even if the United States expands raw material purchases and strategic reserves, dependence on China across intermediate battery materials and finished battery production will remain difficult to unwind. Goldman Sachs likewise noted in a recent report that lithium produced in the United States will inevitably trade at a substantial premium to Chinese lithium because of higher labor costs, stricter environmental regulations and insufficient refining infrastructure. In other words, while the United States grapples with structural cost disadvantages and margin pressure within its emerging domestic supply chain, China is positioned to leverage its superior cost competitiveness to further consolidate its dominance of the global lithium market.

Similar Post