“Extinction Shock Hits Japan”: Population Shrinks 2.5% in Five Years, Vacant-Home Crisis Threatens Regional Finance

Authored On

Modified

Total population falls by 3.09 million in five years as decline accelerates Children aged 14 or younger at 11.2%, people aged 65 or older at 29.4% Regional property markets cool as banks’ earnings base weakens

Japan’s total population has fallen by nearly 3.1 million over the past five years, marking one of the steepest accelerations in its demographic decline. The convergence of low birthrates and population aging has triggered a collapse in regional housing demand and a surge in vacant homes, feeding into falling property values and growing concerns over the soundness of regional banks. Japan’s population decline is now spreading beyond a social issue into a broader risk for capital markets and the financial system.

A More Severe Situation Than Wartime: Japan’s “Extinction Shock”

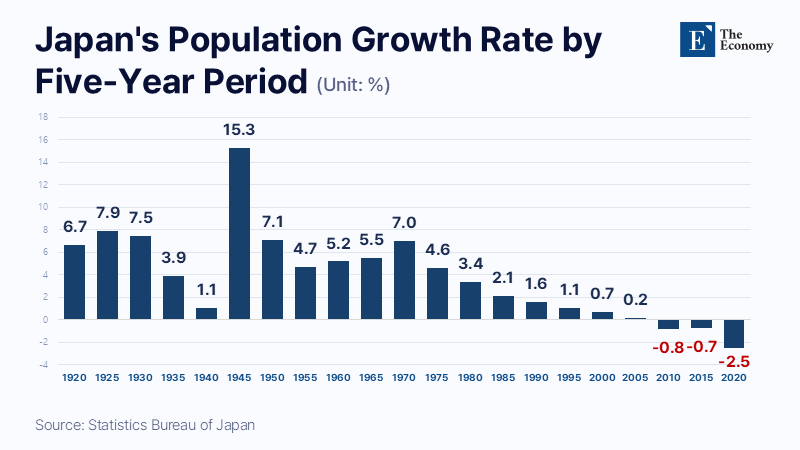

According to preliminary figures from Japan’s Ministry of Internal Affairs and Communications for the 2025 national census released on June 4, Japan’s total population stood at 123,049,524 last year. That represents a decline of 3,096,575, or 2.5%, from the 2020 census five years earlier, the largest drop since the country began conducting population censuses in 1920. It is the first time since the Pacific War from 1941 to 1945 that Japan’s population has naturally declined by more than 3 million over a five-year period. During the war, roughly 3 million people died, including about 2 million soldiers and 1 million civilians.

On the surface, the scale resembles the demographic toll of the Pacific War, but the underlying situation is more severe. The wartime deaths were a temporary shock caused by a single event, while Japan’s current population decline is intertwined with a self-reinforcing structural vicious cycle. After the Pacific War ended, Japan entered a baby boom alongside rapid economic recovery, with the total population rebounding by 15.3%. Today, however, low birthrates and aging are locking Japan into a downward trajectory that increasingly reinforces itself.

The pace of Japan’s population decline is indeed accelerating. The country’s population peaked at 128.05 million in 2010, then began declining for the first time in the 2015 census covering the 2010–2015 period. The decline rate at the time was 0.7%, but the latest census recorded a 2.5% drop. In just five years, the pace of decline has become roughly three times faster.

At the center of this vicious cycle is rapid aging. In the latest census, children aged 14 or younger accounted for only 11.2% of the population, while those aged 65 or older made up 29.4%. In effect, nearly one-third of the population is elderly. By gender, Japan had 59,778,826 men and 63,270,698 women, with the sex ratio standing at 94.5 men per 100 women. As the population of childbearing age rapidly contracts, deaths among the elderly increasingly outnumber births, further accelerating natural decline. Because the generations responsible for future childbirth are becoming thinner over time, the scale of decline is likely to keep widening without a major reversal factor.

Nine Million Vacant Homes, With Some Wooden Houses and Gardens Trading for Under $6,300

This population decline is now translating directly into capital-market shocks. Over the past three decades, Japan’s shrinking population has hollowed out housing demand in regional cities as aging and youth outflows have intensified. Vacant homes have therefore increased rapidly, while daily-life infrastructure has weakened. According to the Ministry of Internal Affairs and Communications’ Housing and Land Survey, vacant homes nationwide totaled 9.002 million in 2023. That equals 13.8% of all homes, with both the number and share reaching record highs. Japan surveys vacant homes every five years, and the figure rose by about 500,000 from 8.49 million homes, or 13.6% of the total, in 2018. Nomura Research Institute projects the vacant-home ratio will rise to 27.3% by 2033.

In Japan, areas with higher aging rates tend to show higher vacant-home ratios. Vacant homes in regional areas have surged as inherited houses are left abandoned after elderly owners die. A 2020 survey by Japan’s Ministry of Land, Infrastructure, Transport and Tourism on vacant-home owners found that inheritance was the most common reason for acquiring a vacant home, at 54.6%.

To address the vacant-home problem, the Japanese government enacted the Act on Special Measures concerning the Promotion of Measures for Vacant Houses in 2015. The law allows local governments to designate buildings that pose safety or sanitation risks, or seriously damage the surrounding landscape, as “specified vacant houses.” Owners of such properties may face phased measures including guidance, recommendations and orders. If owners fail to comply, they must bear demolition costs. If they cannot afford those costs, the land can be put up for public auction. Property owners therefore have to seek solutions, including selling the building, before the problem worsens. The recent rapid increase in vacant-home listings in regional Japan is also seen as partly driven by this regulatory shift. In some regional areas, wooden houses with gardens can be found trading for under about $6,300. There is even a saying that the price of a small studio apartment in Sydney would be enough to buy several rural homes in Japan and still leave money to spare.

Regional Economies Face Collateral Erosion as the Demographic Shock Spreads to Banks

The key concern is that falling regional property values could spread into financial-sector risk. As regional homes shift from tradable assets into liability-like assets that entail management costs, pressure is also building on the soundness of regional financial institutions that have issued loans secured by such properties. The transmission path from Japan’s population decline to regional hollowing, rising vacant homes and ultimately financial-sector risk is becoming increasingly visible.

Japan’s regional banks are particularly exposed because their lending structures are tightly linked to local economies. Regional small and midsize companies, households and real estate-backed loans account for a significant share of their business base. Local population decline therefore simultaneously weakens the deposit base, slows loan demand and erodes collateral values. In regions where younger people have left, demand for new housing falls, inherited homes flood the market after elderly residents die, and the recoverability of properties held as collateral by banks also declines.

The Bank of Japan also recognizes this as a financial-stability risk. In its financial system report last year, the BOJ identified the banking sector’s rising real estate-related lending as a key area for monitoring. While the report assessed that Japan’s overall financial system holds sufficient capital, it warned that a combination of property-price fluctuations, borrower distress and changes in the interest-rate environment could increase pressure on bank profitability and asset quality. The International Monetary Fund also identified the weakening earnings base of regional financial institutions as a vulnerability in its assessment of Japan’s financial system. Japan’s financial sector, led by major banks and insurers, maintains shock-absorption capacity, but regional financial institutions are under persistent pressure from population decline, low growth and limited earnings diversification.

The burden on regional banks does not end with falling collateral values. In regions with declining populations, companies’ revenue bases also weaken. A shrinking consumer population depresses commercial districts, and weaker local commerce in turn undermines the repayment capacity of self-employed businesses and small and midsize companies. If the value of real estate collateral falls while borrowers’ cash flows weaken, banks must build larger loan-loss provisions, which can lead to reduced lending capacity and regional credit tightening. Japanese banks already formed one axis of the country’s prolonged stagnation in the 1990s, when the collapse of the property bubble drove down collateral values and left banks burdened with bad loans. Today’s regional vacant-home problem differs in nature from the speculative bubble collapse of that era, but the financial mechanism in which falling property values weigh on bank balance sheets is similar.

Still, the increase in vacant homes cannot be explained by aging alone. Japanese real estate research institutions analyze that the current surge in vacant homes is rooted in decades of accumulated housing supply expansion. Japan continued building new homes after its high-growth era, and as a cultural preference for newly built homes took hold, the asset value of existing homes declined rapidly. As a result, housing stock exceeded demand in many regional areas even before population decline began in earnest. Statistics from Japan’s Ministry of Internal Affairs and Communications show that the total number of homes has long remained far above the number of households. From this perspective, the rise in vacant homes across regional Japan is both a result of population decline and a legacy of past supply-expansion policies.

Similar Post